In 1999, a virus foreign to North America by the name of West Nile arrived in New York City and then spread across the continent.

Four years later, a previously unknown virus of bats, now infamously known as “SARS”, infected humans in China and then spread to more than two dozen countries, killing 10% of the eight thousand people worldwide that became infected. In 2009, a pandemic strain of the influenza virus known as “H1N1” emerged in Mexico, and then spread to every country in the world in just six weeks. And in the past year, a virus called chikungunya, normally found in Africa and Asia, hit the island of St. Martin, after which it rapidly spread across the Caribbean, and now threatens areas of the continental United States. Today, the largest outbreak of Ebola ever recorded continues to spread widely within three West African countries, recently reaching the large urban centers of Conakry, Freetown and Monrovia.

So why are all these outbreaks happening? Is there just more news of infectious disease outbreaks today, or are they actually increasing in frequency? Confronting these questions requires a look at factors that drive the emergence and international spread of infectious diseases.

Today, a number of global phenomena, from human population growth, to climate change, to surging international air travel, are converging. Foremost, the world’s population is expanding at a rapid pace. With over seven billion people in the world today – half of whom live in densely populated cities – there are simply more opportunities for humans to become infected with dangerous microbes. Consequent to population growth is the growing demand for food. Unfortunately, about threequarters of all new infectious diseases observed in humans have their origins in animals – from SARS, to “bird” flu and even HIV. People tend to become infected with animal pathogens during the production or consumption of livestock or as wildlife ecosystems are disrupted. Furthermore, humans can acquire drug-resistant variants of animal microbes when livestock are fed antibiotics.

While climate change is known to the insurance industry for its impact on the property and casualty market, it sometimes may not be considered in terms of its effect on infectious diseases. Yet many insects from ticks to mosquitoes that can transmit infectious diseases like Lyme or dengue are increasingly able to survive and thrive in areas of the world where the climate is now suitable. In addition to outbreaks resulting from naturally occurring phenomena, the potential exists for microbes manufactured in laboratories to accidentally escape, or more nefariously, for groups to deliberately release biological agents (e.g., as occurred when weaponized anthrax was dispersed via the U.S. postal system in 2001). And with more than three billion trips on commercial flights worldwide every year, humans are increasingly becoming vectors for the spread of infectious diseases by inadvertently transporting dangerous microbes from one region of the globe to another.

The current outbreak of Ebola in West Africa is now larger than all other outbreaks of the disease combined, with more than 2500 reported cases and nearly 1500 deaths. First discovered in Zaire (now Democratic Republic of Congo) and Sudan in 1976, there is currently no vaccine or treatment known to be effective or safe, despite a mortality rate that can be as high as 90%. What makes the current epidemic unique is that while cases of Ebola are typically only found in remote areas, in this epidemic, cases have emerged in large metropolitan centers. This July, an individual infected with Ebola traveled by air from Monrovia, Liberia to Lagos, Nigeria where a cluster of new cases has since emerged among his healthcare providers. These cases and their contacts are being monitored closely with the hopes of preventing further spread in Nigeria. Two U.S. citizens infected with Ebola, who were working in the region, have been repatriated to the U.S. for medical care. Although this has caused some anxiety in the general population, it is important to note that Ebola virus is spread only when uninfected persons come into contact with the body fluids of infected persons. In an industrialized country like the United States, where the risks of new imported cases of Ebola are generally low but not zero, this largely translates into possible exposures to frontline healthcare providers. Since medical and public health systems and hospital infection control practices in the U.S are highly robust, the probability of Ebola virus having an impact among the general population is exceedingly low. For insurers

with critical illness or life exposure in industrialized areas of the world, this knowledge should be balanced against the widespread reporting of Ebola by the global media, to avoid inflated perceptions of risk.

The Recent Threat of Middle East Respiratory Syndrome (MERS)

Caused by a previously unknown coronavirus, MERS was first identified in the Arabian Peninsula back in 2012. Thought to have made the leap to humans from camels, there remains uncertainty as to just how this virus is actually infecting humans. Once humans are infected however, they are able to transmit it from person to person. Fortunately, this virus is far less contagious than its ‘cousin’ of a decade ago, SARS. Largely confined to Saudi Arabia and neighbouring countries, this outbreak has simmered over the past two years. But in the spring of 2014, transmission of this deadly virus – which kills about one third of those infected – increased sharply. While many new infections were related to viral spread within hospitals, the cause of other new infections were unexplained and thought possibly due to contact with camels or unrecognized contaminated areas in the environment. Following this surge in cases came the accelerated international spread of MERS to countries in Western Europe, North Africa, the Middle East, East Asia and even North America (two cases were imported into the U.S.).

What has been challenging with MERS is that there is an incomplete understanding of how it infects humans and, consequently, how best to prevent new infections. Furthermore, it has a broad spectrum of illness, with many of those infected displaying no symptoms at all (incidentally identified when investigating contacts of known MERS cases), others having mild respiratory illnesses that resemble those of common respiratory viruses and, at the other end of the spectrum, severe, life threatening, respiratory failure. While rapid diagnostic tests have been developed to identify the virus in respiratory specimens along with blood tests that can detect evidence of recent infection, not all countries have robust medical and public health systems that can readily detect MERS. Like SARS, what is especially

concerning is that there is no vaccine or effective treatment protocol available (other than supportive management for those who require intensive care).

While many viruses possess the ability to rapidly evolve and take on new characteristics (e.g., become more contagious), fortunately, MERS remains quite limited in its ability to spread from person to person; however, public health

officials around the world are also mindful that Saudi Arabia hosts the largest annual mass gathering in the world. Saudi Arabia, custodian of major religious sites in the Muslim world – the cities of Mecca and Medina – sees about three million pilgrims arrive annually from virtually every country in the world. While international pilgrims arrive throughout the year to perform a ‘lesser pilgrimage’ known as Umrah, numbers increase significantly during the holy month of Ramadan. In October 2014, pilgrims will congregate to perform the Hajj, a mandatory ritual for all physically and financially able Muslims to perform at least once in their lifetime. Given that this congregation involves massive crowds, pilgrims could potentially become infected with MERS in Saudi Arabia, and then develop illness after they return to their home countries. While the recent surge in MERS activity across Saudi Arabia has momentarily subsided, public health officials around the globe, including the World Health Organization, will be closely monitoring the situation leading up to, during, and after the Hajj.

The Power of Predictive Analytics

When infectious disease outbreaks with significant potential health risks arise, how does the insurance industry evaluate them? Is a systematic approach adopted that distinguishes a subjective and potentially emotional driven response from an evidence based, objective assessment of their expected impacts?

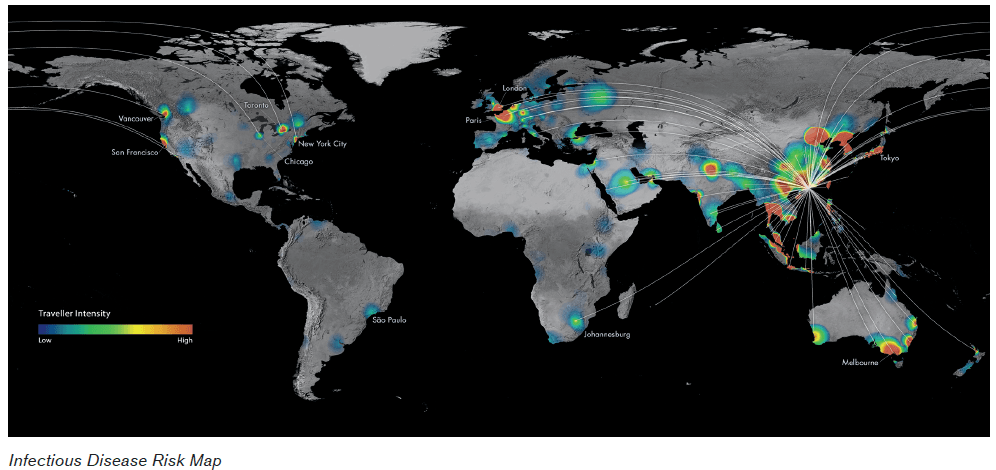

As an infectious disease clinician and scientist at an academic teaching hospital, my perspectives on emerging infectious diseases stem from personal experiences that lie outside of the insurance industry. In 2003, after completing my clinical infectious disease and public health training in New York City, I returned to my home town of Toronto just before SARS made its way to Canada from Hong Kong. It was an eye-opening experience that demonstrated just how interconnected and interdependent our world is when it comes to the threat of infectious diseases. It was also an experience that revealed a major gap in our ability to make informed, time-sensitive decisions about infectious disease threats arising on the other side of the world. Responding to this unmet need, my colleagues and I began integrating our collective expertise in clinical infectious diseases, population and public health, big data, geographic information systems, predictive modeling and web-technology, to develop innovative tools that could help governments better prepare for and respond to the next big infectious disease threat facing their citizens.

After years of building a robust research program and integrating it with the technological know-how to produce timely, scientifically validated predictive analytics, my colleagues and I in academia were well prepared for the H1N1 influenza pandemic of 2009. When we accurately predicted the global wavefront of this pandemic based on analytics of worldwide air traffic patterns (publishing these findings in the New England Journal of Medicine), it became clear that there was a strong interest in anticipating the impacts of globally emerging infectious diseases from both the public and private sectors alike. Maintaining a strong desire for social impact, my colleagues and I founded BioDiaspora – a social benefit corporation – with a mission to prevent or mitigate the health and economic consequences of future infectious disease threats. During the past five years, we have been partnering with key public health organizations in the world like the U.S. Centers for Disease Control and Prevention and the World Health Organization.

An Outsider's View on the Industry

After meeting a variety of insurance industry stakeholders, it did not take long to realize that, when contemplating infectious diseases, a significant amount of time and energy is spent reflecting upon one historical event – the Spanish influenza pandemic of 1918. Even though it occurred almost a century ago – prior to the advent of antibiotics, intensive care units and other modern medical innovations that help keep people alive – it symbolizes a disconcerting and unexpected spike in morbidity and mortality that could have devastating implications to the health of populations worldwide. Thankfully, almost a century later, no other epidemics or pandemics have rivaled the estimated 50-100 million deaths that occurred globally as a result of the Spanish flu; but the memory of this event continues to beg the question, could history repeat itself?

From a biological perspective, it is entirely plausible that a pathogen, comparable in its virulence to the 1918 Spanish influenza virus, could emerge. On the other hand, one could argue that modern antibiotics, vaccines, and life-saving critical care technologies that were not available a century ago, would prevent the sheer volume of lives lost in 1918. But a pragmatist might also remind us that there are limits to supplies of antimicrobials and essential medicines, that significant delays still exist when producing vaccines even for the most common of pathogens such as influenza, and that the finite number of intensive care unit beds cannot easily be increased to respond to a sudden unexpected surge in demand.

With enduring memory of the Spanish flu, it is perhaps not surprising that the insurance industry focuses much of its attention on influenza, a highly unpredictable virus that clearly deserves respect. However, it appears that pandemic influenza has become synonymous with the potential for large-scale morbidity and mortality. But in this subtle assumption lies a possible risk – could a high-impact event arise from pathogens other than influenza? Considering the accelerated emergence of so many previously unknown infectious diseases during the past few decades – many making the leap from animals to humans – it is possible that one of these could be the next “big one”. It is also possible that the world might experience more frequent epidemics in the future, each with smaller impacts than a pandemic, but with cumulative effects on health that could be substantial (epidemics are considered geographically defined events, whereas pandemics are by definition epidemics that spread across the entire world). Considering that present-day scientific knowledge – and future knowledge presumably for some time – is insufficient to anticipate where or when the next influenza pandemic will emerge, just how contagious and deadly it will be, and how well our modern medical and public health systems will be able to respond to it, an important question to ask is just how much energy should be consumed planning specifically for an influenza pandemic?

Infectious Diseases Are Many Things

The term infectious diseases may imply a homogeneous group of illnesses, but in reality they represent a diverse collection of microbes, each with their own unique characteristics, life cycles, and effects on human health. So rather than start with a pathogen – like influenza for example – when evaluating risks to an insurer, perhaps it makes more sense to start with the type of insurance product being considered. For instance, some pathogens can cause chronic morbidity, which could be of interest to those with substantial disability exposure, whereas others are virulent and could pose risks from a critical illness or life perspective.

A geographically tailored method of evaluating risks to an insurer would be to relate its global exposure to a specific insurance product (i.e., life, disability, critical illness) with the global geographic footprints of infectious diseases relevant to that product, while taking into consideration global travel patterns from those infectious disease footprints. Moreover, understanding local context is critical. The observed health impact from an infectious disease is not just a function of the pathogen itself, but also the susceptibility and vulnerability of the population to that pathogen, as well as the suitability of the environment to facilitate pathogen activity. For example, when cholera was introduced into Haiti in 2010 after a devastating earthquake, access to clean water and enhanced sanitation was disrupted, and consequently hundreds of thousands of infections and thousands of deaths ensued. By contrast, if cholera were introduced into a city in the United States where access to clean water and enhanced sanitation was universal, the microbe would quickly be halted in its tracks. So one can see how a single pathogen could have two very different outcomes when context is taken into consideration. Although more complex than focusing on a single pathogen, tailored risk models could be developed that integrate knowledge of worldwide infectious disease activity, global patterns of travel, local population vulnerability and environmental suitability to infectious diseases, as well as an insurer’s geographic exposure by type of insurance product.

Enabling Smarter Decisions

Imagining how big data and predictive analytics could inform smarter decision-making on infectious disease risks facing the insurance industry, it appears that there are opportunities across three time horizons. First, from a long-term perspective (months to years into the future), an insurer could benefit from risk modeling that holistically considers impacts from all relevant infectious diseases in relation to an insurer’s existing (or future anticipated) global insurance exposure (as discussed above). Since global leaders in public health use similar approaches to anticipate future epidemic risks, these methods could be adapted and re-purposed to meet insurance industry needs.

On a nearer-term basis (weeks to months into the future), industry stakeholders could benefit from early warnings of key infectious disease events emerging in the world. As the Internet evolves, it is increasingly used as a crowdsourcing medium for global epidemic intelligence. Since these signals are timely and often precede reporting from official government sources, they can offer valuable insights into potential near-term risks. For example, at the onset of the 2009 H1N1 influenza pandemic, a deviation from the usual seasonal pattern of flu-like-illnesses in Mexico signaled that a possible threat was emerging several weeks before a pandemic risk was formally declared. Although insurers may be limited in their ability to mitigate risks from policies they already hold, timely infectious disease intelligence, coupled with tailored risk assessments, could help inform imminent decisions about new business ventures and opportunities.

Finally, all companies should have robust business resiliency and continuity plans to help them ‘ride the wave’ of an emergency as successfully as possible, whether related or unrelated to infectious diseases. During the midst of a major global infectious disease event, the health and welfare of human resources may be threatened, supply chains might be disrupted (given today’s global nature of business), and decisions about holding capital may arise if an increase in claims is anticipated. Similar to how government health agencies operate, frequent risk assessments based on the most current global information available could help inform short-term decisions (days to weeks into the future) during the midst of an epidemic or pandemic emergency.

Maintaining Perspective

Infectious diseases currently account for about 4% of all deaths in the United States. Although there are far more significant causes of morbidity and mortality across the industrialized world, from vascular disease to cancer and obesity, newly emerging and re-emerging infectious diseases could have significant impacts on the health of populations worldwide over the next few decades. Given that risk assessments in the insurance industry are largely derived from historic data, it is not surprising that there is some discomfort when projecting future risks for major infectious disease events like pandemics, since there are few data points with which to work. This is further complicated by the fact that modern global forces that drive disease emergence and spread are countered by parallel advancements in health technologies that might prevent or mitigate impacts.

Since the recent past might not be predictive of the future when it comes to infectious diseases, the insurance industry may wish to keep key historic events – like the Spanish flu of 1918 – in perspective. Like a brief glance in the rear view mirror, this retrospective look back should not consume an excessive amount of time and energy, since the degree of precision and the answers sought after may simply not be attainable. But adopting a consistent evidence-based approach to evaluating infectious disease risks going forward, that makes creative use of leading-edge science and technology, could help prevent costly inefficiencies that stem from either over-reaction or under-reaction to emerging threats.

Since SARS brought chaos to cities around the world a decade ago, tremendous scientific and technological advances have been made in preparing for the next major infectious disease event. Government health agencies, often in partnership with academia and the private sector, have taken advantage of advances in big data, predictive analytics, web-technology, and data visualization to anticipate the health and economic impacts of future threats. Because the insurance industry also counts lives and impacts to health, there are important opportunities for it to creatively adapt leading innovations to better plan for, become aware of, and effectively and efficiently respond to inevitable infectious disease threats of tomorrow.