Microinsurance, or coverage targeted at financially underserved or low-income individuals, has experienced significant growth over the last decade, and changing distribution models may deserve much of the credit.

But what can these trends teach the industry about closing a persistent insurance gap – even amid a pandemic? New insurance innovations prompted about by the COVID-19 pandemic only emphasize an old struggle to appeal to underinsured and uninsured communities. The evolution of distribution models in microinsurance offers important lessons for all insurers seeking to close this lingering insurance gap.

Recent estimates from Microinsurance Network show that over 280 million people globally are covered by at least one microinsurance policy. This growth is encouraging, but still represents a small fraction of the global potential market estimate of 4 billion consumers. Reaching low-income individuals can be particularly challenging as some may live in rural areas, often lack understanding of insurance, and see insurance products as too complex or expensive. These barriers create a need for innovation, particularly in the distribution and administration of products. Given the low margins, insurers need to partner with aggregators or channels with a large footprint to achieve economies of scale and address high acquisition costs.

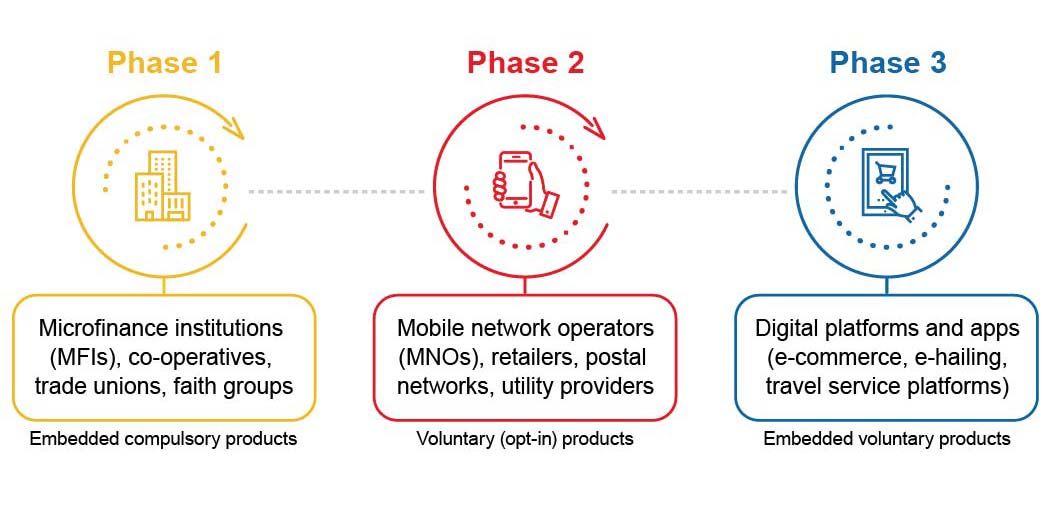

To know where microinsurance is headed and gauge its potential to help close the protection gap, we first need to understand its evolution – both the successes and the missteps. Microinsurance has progressed through three phases; each reveals valuable lessons about reaching low-income, underinsured and underinsured customers. Let's start by going back to basics and exploring what distribution models emerged at each stage:

Phase One: Early distribution models

Interest in microinsurance grew rapidly at the beginning of last decade following the popularity of microfinance across emerging markets. As underserved consumers gained access to loans and other banking services through microfinance institutions (MFIs), there was a natural demand for insurance as MFIs saw the need to protect the book value of loans. Credit life insurance was often embedded in micro-loans, even though customers rarely understood the terms or how insurance worked in practice. Indeed, most customers thought insurance was a requirement for obtaining the loan, resulting in low claims ratios and limited client value. Although concerted strides have been made to increase clients’ understanding of insurance, most MFIs have been slow to move beyond mandatory products (typically embedded in loans) to voluntary products that provide better value for clients.

Besides MFIs, the early distribution models for microinsurance also relied on community-based organizations such as cooperatives, trade unions, and faith-based groups. These traditional establishments typically have a strong social mission and are widely known and trusted in low-income communities. They also tend to have a large base of members and often have existing infrastructure to facilitate the administration of policies. Indeed, the landscape studies across different emerging markets indicate that MFIs and community-based organizations have remained the most dominant distribution channels for microinsurance.

Despite the benefits of traditional channels, limitations such as lack of product awareness and insurance culture, low claims ratios, difficulties in pivoting to voluntary products, and regulatory constraints have impeded the ability of microinsurance to scale to the extent anticipated.

Phase Two: Evolving distribution models

How have distribution models changed in the last decade? Rapid mobile technology advances in emerging markets have created openings for new distribution models and significantly changed the landscape and growth of microinsurance. For example, sub-Saharan Africa is reported to have the fastest-growing mobile economy in the world, with mobile penetration growing from 280 million subscribers in 2012 to more than 456 million in 2019. It is predicted to reach around 623 million subscribers in 2025 (around half of Africa’s total population).

With millions of subscribers, mobile-based distribution networks promised strong opportunities to scale, capitalizing on the subscriber’s trust of each Mobile Network Operator (MNO) brand. In addition, the use of relatively low-cost mobile channels offered the potential to reach poorer and more remote clients. Through mobile technology, MNOs could effectively facilitate various processes ranging from payments to administration and client servicing. The GSMA reports that there are currently 102 mobile-enabled insurance services in 27 countries. Interestingly, the early mobile microinsurance deployments were driven by insurers looking to extend into the lower-income segment, but the more recent deployments are being largely driven by MNOs seeking to reduce churn and increase customer loyalty in highly competitive voice markets.

During the last decade, the market also witnessed the emergence of mobile microinsurance intermediaries. These companies understand the insurance industry – knowledge many MNOs lack – and know the low-income customers that make up the target market, information that insurers lack. As a result, these intermediaries link the consumer, MNO, and the insurer. In addition, they provide the technology (insurtech) platforms that facilitate product development, premium collection, and claims administration. In some jurisdictions, these intermediaries may be licensed as risk carriers, offering their own products to consumers. Indeed, mobile microinsurance intermediaries have been able to scale, with most signing up millions of customers within a relatively short period, leading to a massive increase in the number of lives covered by microinsurance globally.

As mobile microinsurance evolved, three distinct business models emerged in the market – loyalty, freemium, and paid models:

- In the loyalty model, subscribers receive ‘free-embedded insurance’ in proportion to the amount of airtime used as a loyalty benefit.

- The ‘freemium’ model allows subscribers to upgrade their loyalty (free) insurance cover for a monthly fee.

- The paid model offers standalone voluntary cover in exchange for premium payments made through airtime deduction or mobile-money wallets.

Basically, the hypothesis was that subscribers would experience insurance for the first time via loyalty or freemium insurance, for a specific period, and thereafter voluntarily upgrade to a paid product.

Besides MNOs, other ‘mass-market’ channels – such as retailers, utility providers, post offices, etc. – were utilized by insurers to distribute microinsurance products. These mass-market distribution channels were often trusted brands and enjoyed a high degree of popularity in the low-income market, thus offering the opportunity to achieve scale by providing access to their vast pool of clients and infrastructure footprint. In most instances, these channels have existing transaction platforms that could be leveraged for premium collection. Furthermore, products sold through mass-market channels are typically voluntary products where a customer has the choice to explicitly ‘’opt-in’’ for the insurance benefit. The opt-in principle also applies to the loyalty (free) products offered by MNOs.

Although mass-market channels offer an attractive way to target a large pool of clients, they are not without challenges. These channels are traditionally not in the insurance space and often offer microinsurance products as a value-added service to increase customer loyalty. Indeed, insurance faces stiff competition for consumer dollars when compared to other, more tangible value-added services (such as retail vouchers, ringtones, streaming services, etc.) offered by the mass-market channel.

Despite access to mobile technology, insurers are face challenging client interaction and premium collection issues, as well. For example, in certain markets MNOs are not permitted to provide insurance advice or automatically deduct premiums (via airtime or mobile money) due to regulatory restrictions. In some instances, payment issues were caused by the lack of commitment from the MNO in integrating the payment infrastructure with the insurer. Given that the channel typically owns the client data and relationship, the success of a microinsurance campaign is dependent on trust and alignment of interests between the insurer and the mass-market channel.

Interestingly, towards the end of the last decade the number of lives covered by microinsurance decreased. This downward trend was primarily driven by partnership issues. Some mobile microinsurance schemes were discontinued or phased out, which led to millions of subscribers losing their insurance coverage practically overnight due to strategic issues between the MNO, the insurer, and intermediaries. Furthermore, a recent study by the Microinsurance Network reports the closure of several mobile microinsurance schemes in Africa due to the unsustainability of the freemium model; most insurers struggled to convert their loyalty-based and freemium customers to paying accounts.

Phase Three: Distribution models of the future

In recent times, the microinsurance landscape has been transitioning away from mobile sales as insurers explore other customer aggregation channels, such as digital platforms and apps. These platforms typically bring together buyers and sellers of goods and services by allowing them to digitally and seamlessly transact with one another. The explosion of big data, artificial intelligence, and insurtech has given rise to the emergence of platforms economies such as e-commerce, e-hailing, and travel service platforms across emerging markets. China is considered a global leader in e-commerce with more than 800 million digital consumers, accounting for $1.5 trillion in online retail sales. In sub-Saharan Africa, digital platforms are continuing to expand at a rapid pace, with more than 365 unique digital platforms and an average of 1.2 million active consumers annually.

Digital platforms have a large, and growing customer base with established presence and trust among platform participants. In addition, digital platforms support a wide variety of payment mechanisms such as mobile payments, digital wallets, cash, bank transfer, credit or debit card, and cryptocurrency. These schemes can seamlessly facilitate transactions across the financial services value chain. Indeed, the unique characteristics of digital platforms provide a strong motivation to partner with insurers to offer products to underserved consumers in emerging markets.

The effectiveness of digital platforms as a viable distribution channel for microinsurance is still in the proving stage, and questions remain as to whether these platforms can scale and aggregate the right type of customers, and if insurance aligns well with other products being offered. Nevertheless, the market seems quite optimistic about the potential of digital platforms given that they can offer better aggregation, payment flexibility, and seamless integration. Because digital platforms facilitate operations with a wider ecosystem of partners, it is hoped that the incentives of digital platforms and insurers become better aligned to ensure the design of valuable products that meet the needs of the low-income market.

Conclusion

Distribution, often described as the ‘toughest nut to crack’, is essential for the long-term viability of microinsurance. The last decade has been characterised by exciting innovations brought about by mobile technology. Interestingly, the initial excitement around high take-up rates for mobile-distributed products, followed by disappointing low retentions, highlights the importance of client education and alignment of interests with distribution partners. The distribution models for microinsurance seems to have come full circle with providers moving beyond voluntary, mobile-based products to embedded products sold through digital platforms which can seamlessly integrate flexible payment methods across the value chain. As rapid digitisation becomes necessary for both insurers and consumers on the back of COVID-19, it is hoped that these new distribution models take the market a step closer to closing the insurance gap for low-income consumers.