A successful underwriting career requires the ability to understand and effectively address a situation based on all available information.

Underwriters must organize facts, sort data, and assess information to define a problem and develop effective solutions. These skills, which underwriters use on a daily basis to make decisions, can all be grouped in the category of critical thinking.

This final installment in a three-part series of articles, which also includes Part I: The Evolution of Decision-Making Thought Processes and Part II: The Role of Heuristics and Neutralizing Bias in Critical Thinking, focuses on identifying critical thinking skills and ways to develop them.

What Is Critical Thinking?

Critical thinking is defined as the analysis of facts, findings and observable phenomena to form a reasoned judgment. Good critical thinkers can draw reasonable conclusions from limited information and distinguish between useful and less useful factors when making decisions. Critical thinking requires higher-order thinking skills, not just memorization or acceptance of what we read or are told. Perhaps more importantly, critical thinking can be continually improved.

See also: Thinking about Critical Thinking in Insurance Underwriting

Can Critical Thinking be Learned?

Critical thinking is a product of education and practice. Although many underwriters are naturally inquisitive, training is required to become systematically analytical, fair, and open-minded in how they do their work. Objectivity is essential: Analyzing a situation without allowing emotions, assumptions, or biases to influence thinking is a professional responsibility. Some individuals are inclined to adopt critical thinking skills early in their careers, while others may take longer to achieve this level of decisioning proficiency. The process requires understanding the basic habits of thought required and applying those habits to underwriting.

See also: Understanding the Evolution of Underwriting

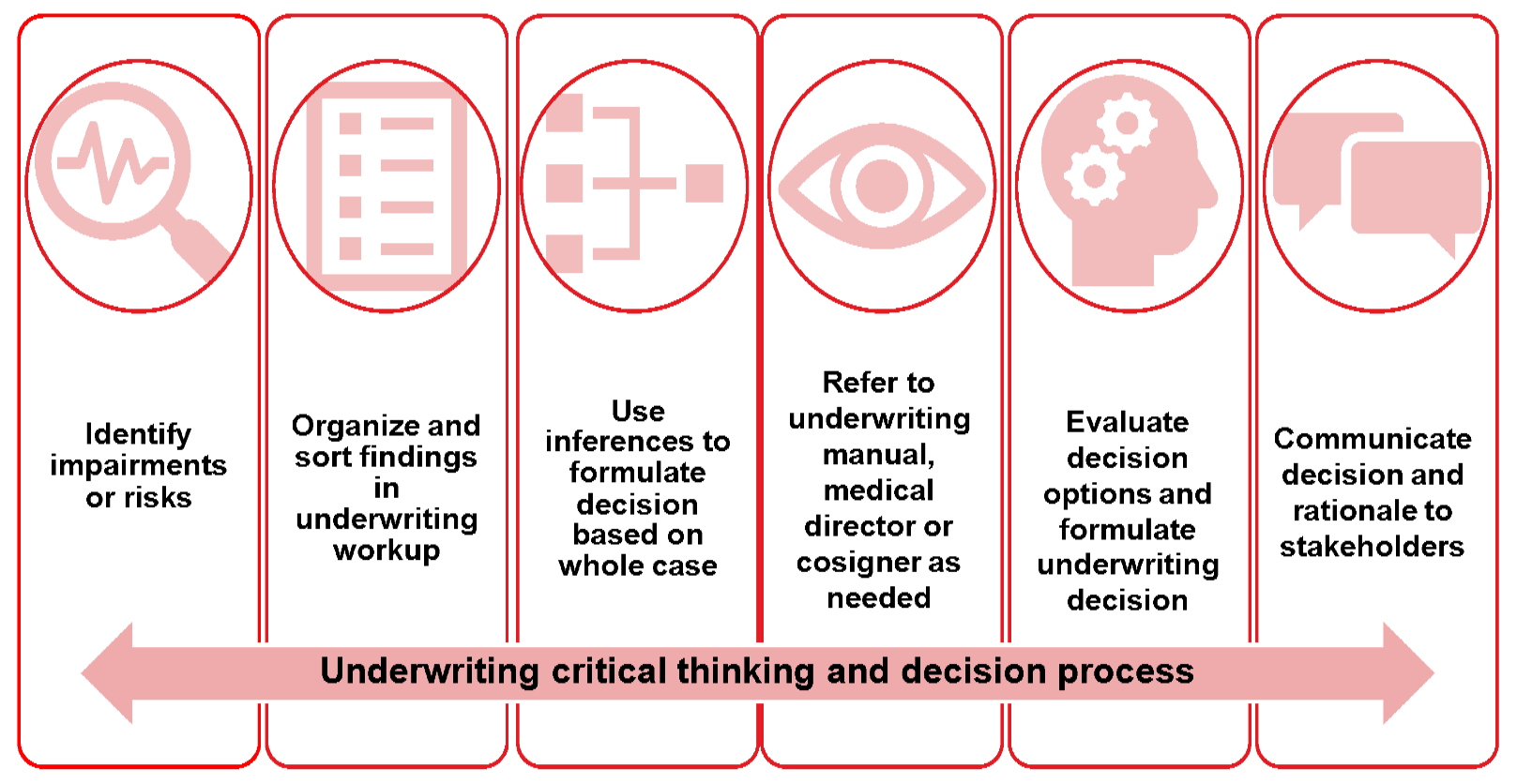

What Are the Skills Essential to Critical Thinking?

Moving through the steps above requires a set of critical thinking skills that underwriters spend their careers perfecting:

- Observation: Critical thinking starts here. Observant and experienced underwriters can quickly identify a new problem, understand why it developed, and even predict when a future problem might occur.

- Analysis: The ability to analyze a situation and quickly identify facts, data, and important information is an essential problem-solving skill for underwriters.

- Inference: When provided limited information, an underwriter must sometimes make inferences to fill in the gaps in reaching a decision – a skill developed over time based on individual experience, technical industry knowledge, and observed outcomes.

- Open-mindedness: An underwriter must put aside assumptions, judgements, and biases in conducting reviews, a practice that can be cultivated through regular training, testing, and auditing.

- Communication: Communication skills allow underwriters to articulate their thinking as they prepare to discuss issues and explain possible solutions to stakeholders.

- Problem-solving: After the problem has been identified and analyzed and possible solutions have been considered, the final step is to execute the solution. This is an area where consultation with senior underwriters can provide vital insights for complex cases.

How Can Insurers Cultivate Critical Thinking?

Insurance companies that cultivate critical thinking skills in their underwriters through practice and extended educational opportunities are making a sound investment in their future. The following steps can help improve critical thinking in underwriting:

- Expand industry-specific knowledge. This can include subjects such as the regulatory landscape, wording of contract provisions, benefit definitions (e.g., definition of disability or total and permanent disability), and market-specific drivers.

- Work with a mentor. Together discuss the key aspects of complex cases and the potential outcomes to determine the best decision given the specifics of the situation. For example, if additional requirements are suggested, evaluate whether these requirements will add value and change the overall outcome of the case. The ability to foresee various outcomes based on information obtained is key to managing risk.

- Consider different possibilities. Practice writing concise underwriting workups, focusing only on the specific problems/impairments on a case. Brainstorm potential solutions and think about the case from various angles so the nature of the thought process is non-binary and not just yes or no. Think: How can an offer be made on this case? This process is the key to developing advanced underwriting skills.

- Practice making decisions. Make decisions or recommend solutions for every cosigning or medical referral, especially on cases that include impairments not seen previously. If an underwriting referral does not include a decision or suggested decision, mentors/cosigners should return the case to the underwriter for his/her decision rather than continuing the review and making a final decision.

See also: Art or Science? Cultivating the Next Generation of Underwriting Talent Holds the Key

Conclusion

Critical thinking in underwriting can be learned. It starts with remaining grounded in facts and knowing there are always opportunities to improve. A multifaceted approach to underwriter training is the way forward – an ongoing team effort that enables the underwriter to become future-ready more quickly. In developing talent, tapping into industry resources and training materials is a good first step. Consistent mentoring by senior professionals is another essential ingredient in the recipe. Finally, opportunities to rotate among different teams and gather diverse experiences offer a powerful means to develop tomorrow’s underwriting superstars.