It's a challenging, and yet also exhilarating, time to be an underwriter in the U.K. and around the world.

New technologies are rapidly transforming how consumers access healthcare services and what consumers expect from their insurers.

The result is rising pressure on underwriters to provide smarter, more competitive decisions faster. Bedrock beliefs about data-gathering are being challenged as insurers ask whether current underwriting processes are still fit-for-purpose and question whether accelerated underwriting could increase non-disclosure risk.

The time is right to "future-proof" underwriting processes. Let’s consider six key facts:

1. Market disruption is happening now

Major changes include:

- More consumer access to digital health technologies, including increasingly sophisticated wearable devices and smartphone apps

- Direct-to-consumer testing, walk-in clinics, and online private general practitioners (GPs) with video consultations

- Higher straight-through point-of-sale processing rates, with ever greater reliance on customer disclosure even for serious medical conditions

- Product developments, particularly for numerous new critical illness conditions

- Signature-less electronic application forms

Of particular concern is the plethora of available online and digital medical services, such as:

- Gene testing: consumer genetic testing services such as 23andMe, Color

- Lifestyle tests: HIV and STIs

- Smartphone apps: Single-lead electrocardiograms (ECGs), melanoma detection, ‘symptom checkers’

2. As the applicant gains access to more knowledge, the anti-selection risk grows

How far has the balance of knowledge shifted towards the applicant, and can we allow it to continue before we change underwriting practices? Could such changes create an environment where misrepresentation could flourish?

Although we expect the GP report to remain the optimum method for medical information, its ability to provide a complete picture is weakening.

Potential solutions include changes to application forms, using information from non-traditional sources, and increasing the use of electronic health reports.

3. Non-disclosure is nothing new

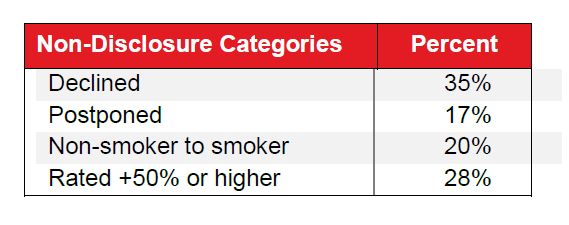

Non-disclosure has always been a challenge for the industry; a recent RGA study has confirmed this is still true.

Post-issue GP reports were obtained on more than 2,000 cases accepted at standard rates for life cover in the U.K. Our study found a 9% material non-disclosure rate, with 52% of cases with non-disclosure subsequently declined or postponed.

Non-disclosure of serious medical conditions is still a significant problem and is likely to worsen. Is it time for our industry to take a fresh look at underwriting processes and how we can adapt?

4. Application forms need to be modernised

RGA conducted an in-depth review of a broad selection of current application forms. The review found a distinct lack of questions about self-testing, private consultations, or indeed any forms of digital health technology. Additionally, current application form questions, supporting help text, and guidance notes were not designed with non-traditional access to health services in mind.

Perhaps a first step could be to review application forms for ‘quick win’ changes; e.g., revise question wordings. Updates to supporting help notes, consents, and declarations could also help applicants to understand what they need to tell us.

All of this applies to online applications as well. There is a growing opportunity to make interactive underwriting more detailed.

5. Underwriting processes will need to include non-traditional data sources

Data from non-traditional sources could help applicants avoid the pitfalls of non-disclosure. Non-traditional information sources can include:

- wearable devices

- smartphone apps

- social media

Accessing such information is not yet straightforward and is likely to entail major changes to processes. We also need to ensure appropriate consents are obtained and to provide sufficient information about how the data will be used.

6. Electronic health reports will become increasingly crucial

Technological advances by the U.K.’s National Health Service are creating new opportunities to obtain medical evidence. Easier access to electronic health reports, particularly post-issue electronic reports, could allow radical changes to the application experience for life insurance customers.

Looking ahead

Only the most agile insurers will be able to cope with the pace of change and newer challengers. Those that cannot adapt underwriting processes could find themselves discussing the need for significantly lower non-medical limits or big increases to premiums.

As insurance applicants become more and more informed, anti-selection risk is increasing. At the same time, these changes offer opportunities to obtain information directly from applicants.

At RGA, we believe these changes present opportunities to examine and risks to manage. Contact our U.K. team to discuss what options work best for you.