In 2018, RGA’s Healthcare Turnkey (HCTK) division surveyed reinsurance broker partners about the self-funded market to gain insights into market trends and drivers.

The 2018 survey findings revealed a strong interest among health plans in being able to offer self-funded insurance. Primary drivers behind this trend included goals to grow and retain business as well as the desire to minimize costs by steering members to the health plans’ network providers and facilities.

In 2020, RGA invited key brokerage firms to participate in an online survey to gauge the interest of healthcare provider organizations in self-funding. According to the brokers surveyed, healthcare provider organizations seeking to potentially enter the self-funded market seem to be motivated by some of the same drivers revealed in the 2018 survey, including a desire to drive members to their own networks. This report reflects input from the nine survey respondents, which include some of the largest brokerage firms in the industry.

Provider Clients: Self-Funded Products – Offerings and Interest

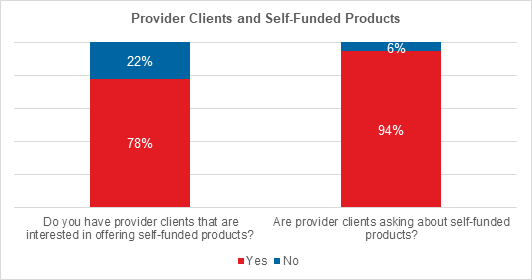

The brokers surveyed indicated a strong level of interest in offering self-funded products among their provider clients. 94% of brokers have provider clients asking about self-funded products, and 78% have provider clients interested in offering self-funded products.

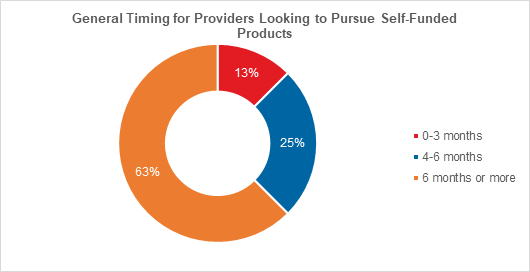

44% of respondents indicated that pursuing self-funded products was a top or moderate priority for provider clients. Of that group, 25% are looking to pursue self-funded products in the next four to six months and 63% are looking to pursue self-funded products in six months or more. This represents a current emerging market and substantial opportunity in the next year and beyond.

Entering and Succeeding in the Self-Funded Market

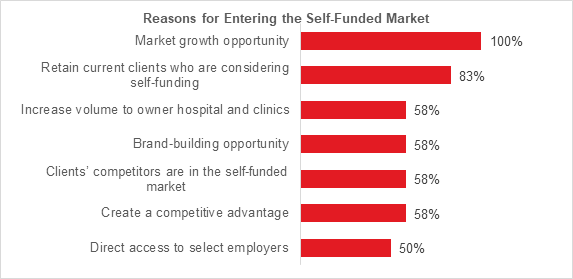

All respondents selected market growth opportunity as motivation for their provider clients who have entered the self-funded market. Retaining current clients considering self-funding was the second most common reason. Keeping up with or ahead of the competition is another common motivator for clients who have entered the self-funded market, as indicated by 58% of respondents.

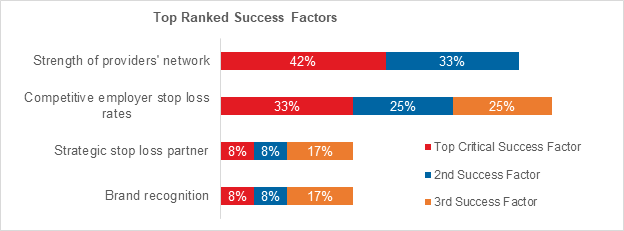

When asked to choose the top three success factors for providers entering the self-funded market, 75% of brokers selected the strength of providers’ network as the top or second most important success factor. Brokers view the strength of the network and the strength of rates as critically important. Competitive employer stop loss (ESL) rates were ranked first or second by 58% of brokers.

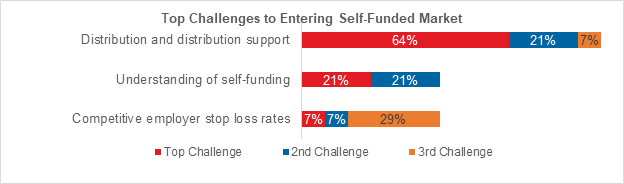

Provider Clients Wanting to Enter the Self-Funded Market

Brokers were asked to list the top three challenges faced by provider clients wanting to enter the self-funded market. Distribution and distribution support were identified as the top challenges by a considerable margin. In order to successfully enter the self-funded market, provider clients need a strategic partner to help with distribution and distribution support. Understanding of self-funding and competitive ESL rates were noted as the second and third biggest challenges, underscoring a need and opportunity for education and training. A dedicated stop loss partner ranked as the fourth biggest challenge.

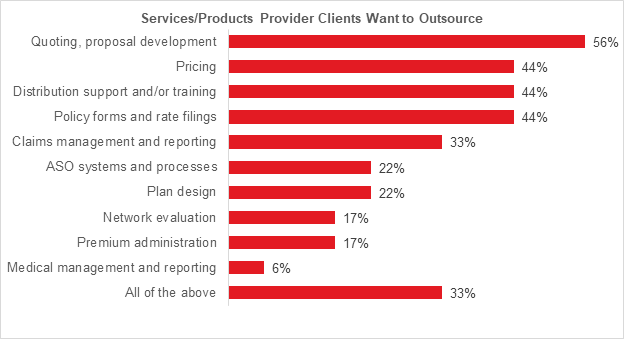

Interest in a Complete Turnkey Solution and Outsourcing Services

Brokers were also asked to provide their opinion on which services or processes provider clients would want to outsource in order to succeed in the ESL and self-funded markets. 56% identified quoting and proposal development, followed by pricing, distribution support and/or training, and policy forms and rate filings at 44% each. Notably, 33% selected “all of the above,” showing a possible high demand for a comprehensive package of services for providers to enter the self-funded market.

78% of brokers responded that a complete ESL turnkey solution would be very valuable or valuable to provider clients. Several brokers commented that self-funding is a growing market in which providers want to participate and a stop loss turnkey solution may be the best viable option for many provider clients to do so.

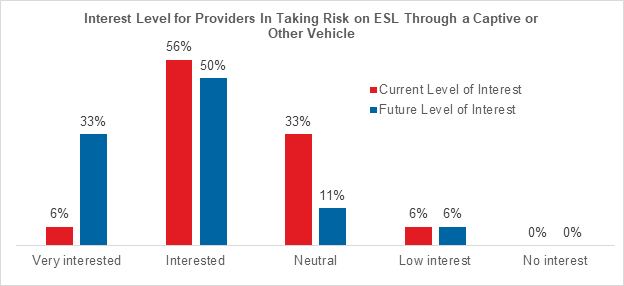

Broker Feedback on Provider Clients’ Interest in Taking ESL Risk

Brokers were asked whether they thought providers would be interested in taking on ESL risk through a captive or another vehicle. Over 60% feel providers are interested or very interested in taking ESL risk today and that 83% will be interested or very interested in doing so in the future. Comments indicated that more forward-thinking or sophisticated providers already see the value, and brokers expect other providers will move in that direction if they believe it will be profitable.

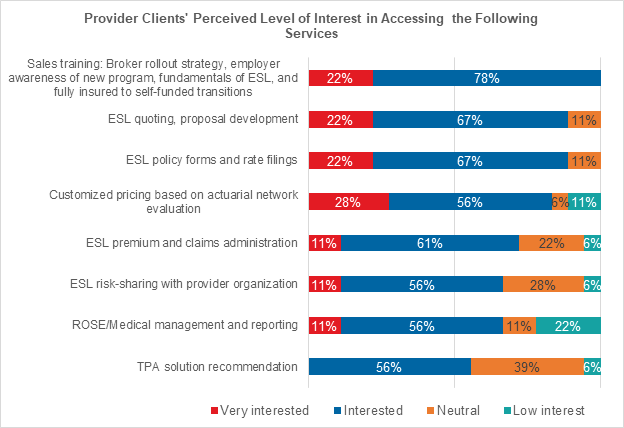

Support Through a Suite of Managing General Underwriter (MGU) Services

All brokers said that provider clients would be interested or very interested in sales training – meaning broker rollout strategy, employer awareness of any new program, fundamentals of ESL, and fully insured to self-funded transitions. ESL quoting and proposal development, ESL policy forms and rate filings, and customized pricing based on actuarial network evaluation were also highly rated as services that clients would be interested or very interested in. The strong level of perceived interest in all the services listed may indicate an opportunity for a comprehensive suite of services. One broker commented that some provider groups are looking for a collaborative relationship and not looking for a reinsurer to “drive the train.” Alternative risk sharing arrangements and a wrap network were other services mentioned that had not been included in the survey.

67% of brokers said that the availability of a full suite of ESL and MGU services for the provider market – third party administrator (TPA) partners, administrative services only (ASO) partner recommendations, sales training and distribution services, and network evaluations – would be a meaningful or very meaningful opportunity for their business.

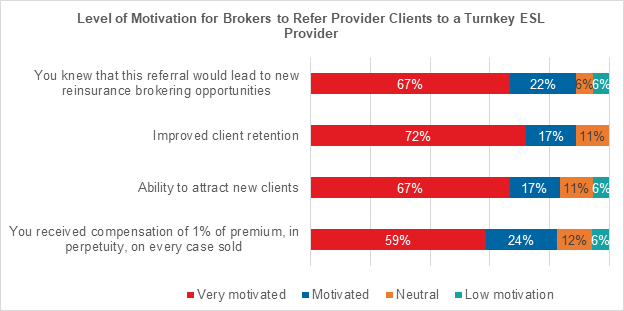

Broker Motivation to Refer Provider Clients to a Turnkey ESL Provider

We asked brokers what would motivate them to refer provider clients to a turnkey ESL provider, recognizing that they would not be handling the day-to-day stop loss quotes. 89% of brokers said they would be motivated or very motivated by knowing that the referral would lead to new reinsurance brokering opportunities or by improving client retention. The ability to attract new clients and compensation (1% of premium on every case sold in perpetuity) were also regarded as motivating or very motivating by most brokers.

The survey results reaffirm that to succeed in entering the self-funded market, providers can benefit from a strategic partner to help with distribution support, as well as a comprehensive package of services.