Digital innovation within insurance distribution is moving at a rapid pace. Life insurers are aiming to meet the rising bar of higher service standards and growing customer expectations.

Earlier this year, RGAX conducted research through the online survey “Digital Distribution: 2018 Pulse of the Industry,” targeting small-to-medium-sized U.S. insurers. The goal was to provide a current outlook on the level of education and capabilities within the digital marketing space for insurance. This report features telling insights from survey respondents on how they currently engage with digital marketing tools, partners, and vendors. It also overviews potential enhancements to the customer experience and additional opportunities for growth and scalability.

Products and Channel Marketing

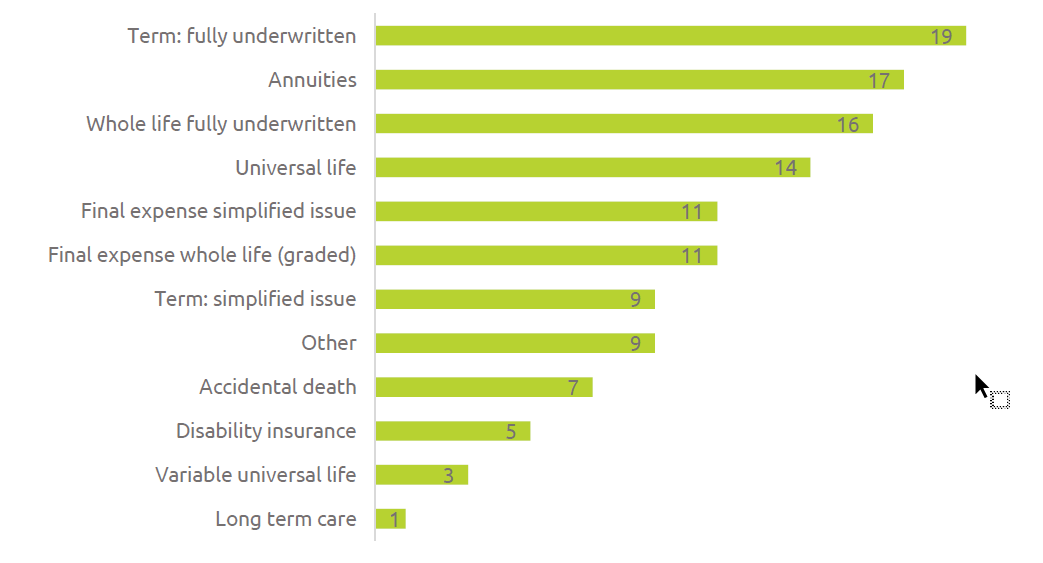

For existing product offerings, term products fully underwritten garnered the most responses and are currently marketed by 19 (out of 25) carriers1. Annuities ranked as the second most popular product, marketed by 17 respondents. Next came whole life fully underwritten products (16) and universal life (14). Less than half of respondents indicated marketing any one of the remaining products, which included digital distribution: final expense simplified issue (11); final expense whole life (11); term: simplified issue (9); accidental death and disability insurance (5); variable universal life (3); and long-term care products (1). Nine respondents indicated marketing a product other than the types listed here.

Figure 1: Current Products Marketed by Carriers (25 Respondents)

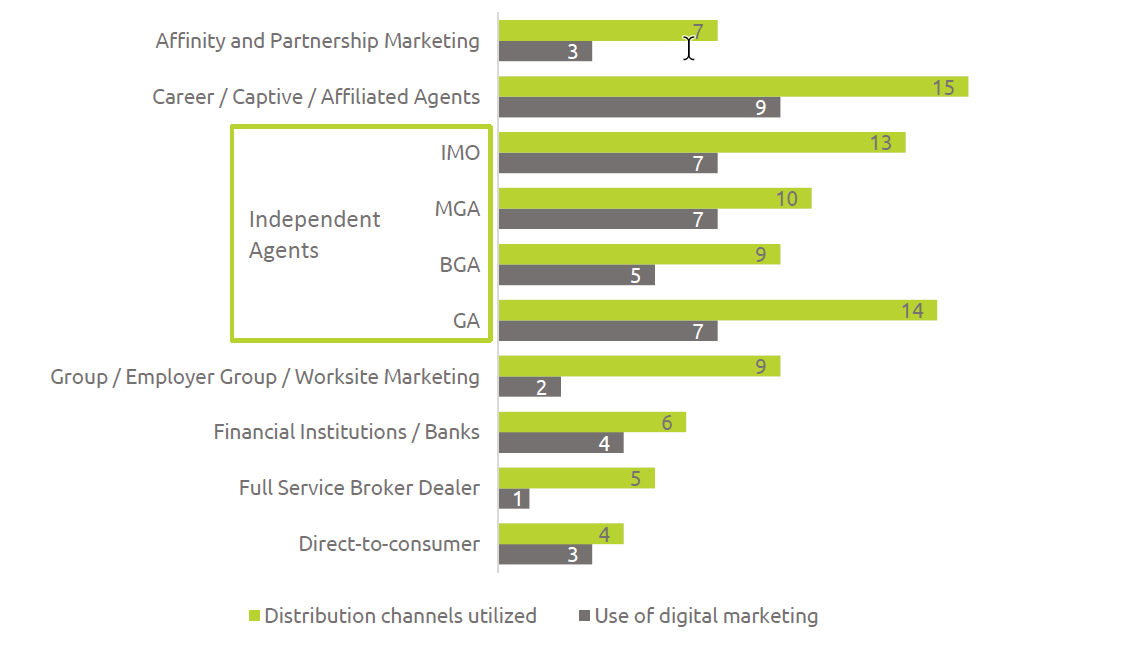

Use of Digital Marketing by Channels of Distribution

As referenced in Figure 2, career, captive, and affiliated agents represent the channel with the highest reported utilization with 15 respondents using this channel. A range of independent agents followed, including general agents (GAs – 14 responses), independent marketing organizations (IMOs – 13 responses), managing general agents (MGAs – 10 responses), and business general agents (BGAs – 9 responses).

Nine carriers reported offering products through their group, employer group, and worksite marketing channels. Affinity and partnership marketing is used by seven respondents, while banks and financial institutions were reported as viable channels by six respondents. Only five of 25 carriers reported using a full-service broker dealer and just four a direct-to-consumer channel.

The use of digital marketing mirrored the channels utilized but with lower numbers in total. The largest differences between the number of respondents using the channel and the number using digital marketing could be found among GAs (14 vs. 7) and group/employer group/worksite marketing (9 vs. 2).

Figure 2:

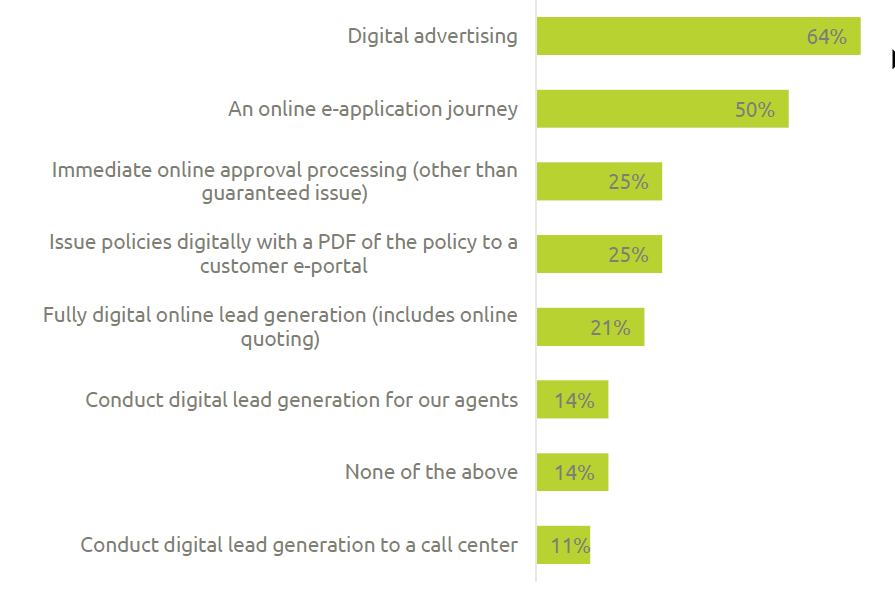

Lead Generation: Current Progress for Testing Direct-to-Consumer Digital Marketing

Of the 28 survey respondents, 64% reported that they are currently testing digital advertising, and 50% are testing an online e-application journey. Refer to the graph displayed in Figure 3.

One quarter (25%) of participants indicated that they are testing immediate online approval processing (other than guarantee issue), and the same percentage are testing issuing policies digitally with a PDF of the policy to a customer e-portal. Additional D2C strategies include fully digital capabilities for online lead generation (21% of respondents testing) digital lead generation for agents (14%), and digital lead generation to a call center (11%). Interestingly, 14% indicated that they have not made any progress for any of the categories listed in the survey.

Figure 3:

Progress for Testing D2C Marketing

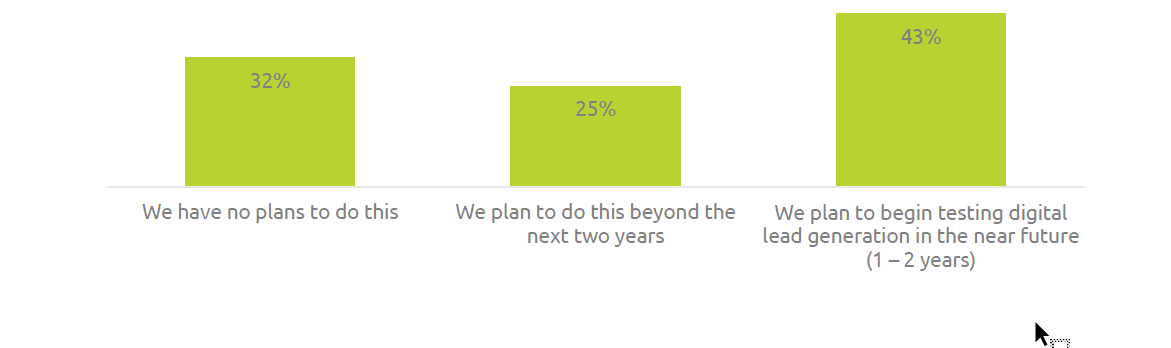

Future Planning for Lead Generation

For most participants (about two-thirds), future planning for digital lead generation is underway, with 43% of the survey respondents planning to begin testing with the next two years and 25% expecting to pursue lead generation beyond the next two years.

Figure 4:

Testing Digital Marketing

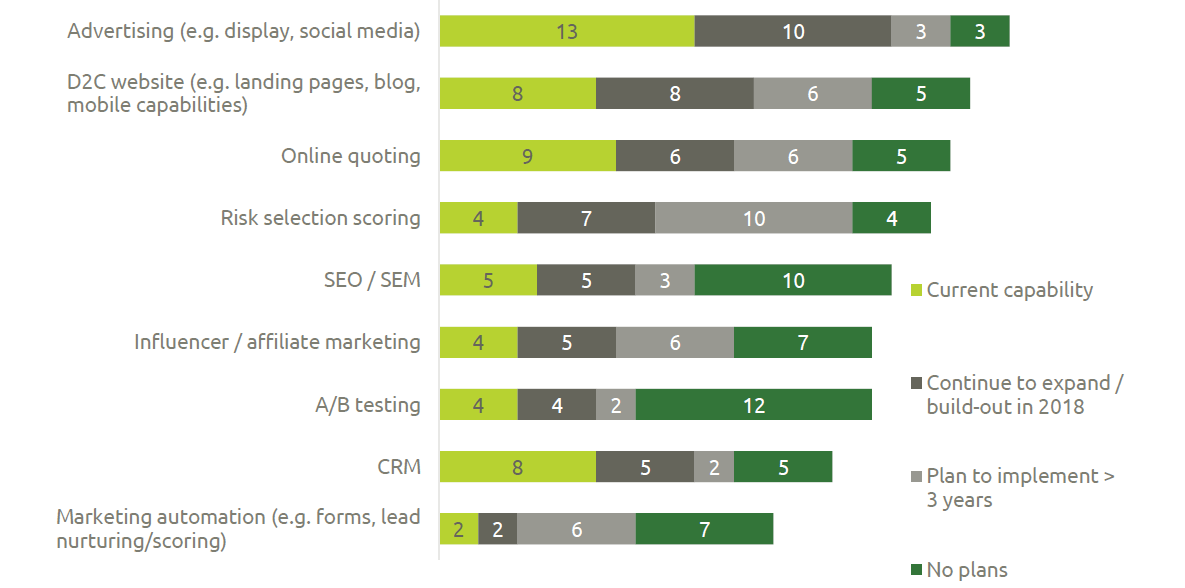

Figure 5:

Not unexpectedly, the largest group of respondents (13) currently have testing capabilities in place for advertising (e.g., display and social media) as it is the most readily available digital strategy.

Another 10 participants plan to continue to expand or build out these services in 2018. D2C web activities, such as landing pages, blogs, and mobile testing, are currently in place for eight companies with another eight having immediate plans to implement. Current testing for online quoting is in progress for nine participants, and another six have short-term goals to get started. Eight participants reported CRM capabilities with another five having CRM expansion plans in 2018.

It is interesting to note that A/B testing was not a more pervasive capability. Tech leaders like Netflix provide a strong example of how insurers could be adapting technology with the goal of increasing customer engagement and satisfaction. Netflix’s competitive advantage stems from its large-scale investment into understanding how customers engage with its products and innovations. Netflix conducts rigorous A/B testing to determine how consumers respond to product changes, personalized homepages, and UI designs. This strategy has proven effective, and insurers might consider incorporating a similar approach into their digital strategies.

Insurers have typically developed products based on the rules of compliance or actuarial requirements rather than through insightful research into customer preferences. Customers are more likely to be engaged in a sales process that is visually appealing and attractive on an emotional level, or that delivers optimized marketing messages uniquely relevant to them.

There is a correlation at successful companies between high customer satisfaction and high profit margins. The insurance industry has much to learn from innovators like Netflix.

Online Application Processing

For the small-to-medium-sized carriers seeking new strategies for e-application processing, 21% reported partnering with startups or external partners. Another 43% of respondents indicated that they did not currently have any active partners or partnerships for this function, but were exploring or planning to partner in the future. The remaining 36% reported no interest.

Partnerships provided respondents with the following key ways to enable e-application selling strategies:

Improved mobile delivery options

Development of D2C and accelerated underwriting platforms

Ventures with insurtech startups

Greater flexibility with multiple vendors for broker partners

E-application support (e.g., iPipeline)

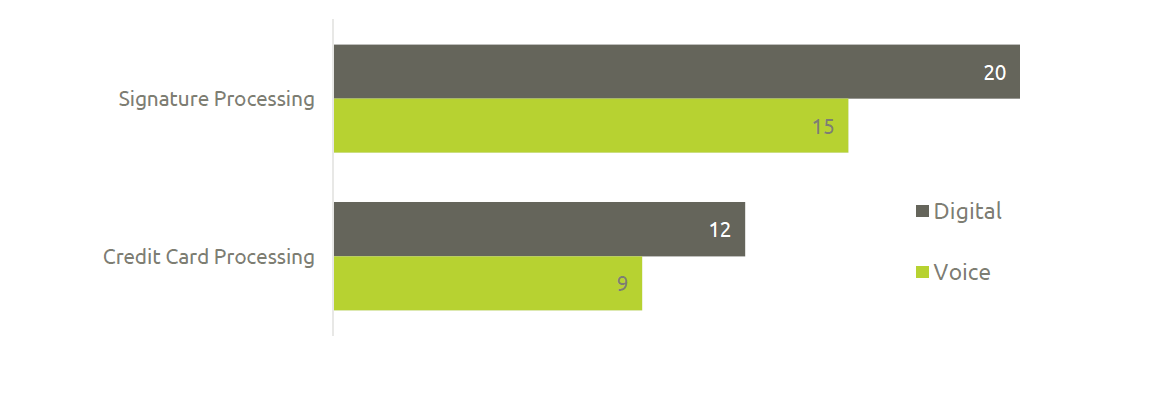

Signature and Credit Card Processing Capabilities

Increased capabilities such as signature and credit card processing make the customer journey smoother and more convenient for those buying insurance.

Our survey findings reflect that the majority of 23 respondents, 87%, offer digital signature processing, while 65% offer voice signature processing capabilities. Credit card processing lagged slightly behind with only 52% offering digital capabilities and 40% using voice commands. Please see Figure 6 below.

Figure 6:

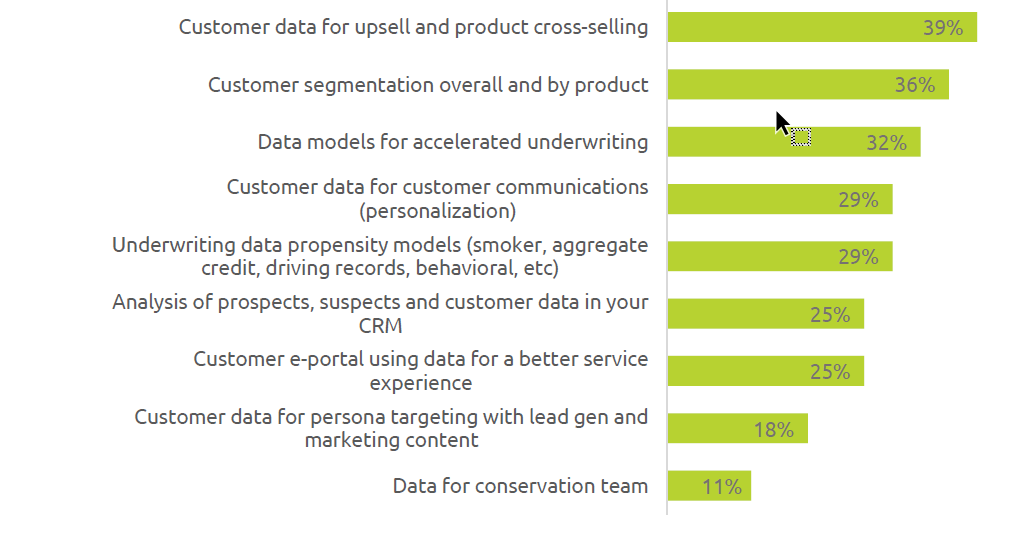

Data and Risk Selection

Despite the continuous “buzz” around using data to enhance insurance sales strategies, our survey findings did not yield a high number of respondents currently using data with a customer focus, suggesting this may be an area for growth. Respondents to this question indicated a broad range in the number of strategies they are employing. Meanwhile, one carrier reported “this is exactly where we fall short” and another is “just starting to talk about this now.”

The use of only one data strategy was reported by 46% (of 26 responses), while 15% reported using two and three strategies respectively. 8% reported implementing four data strategies with a customer focus, while 4% of insurers use five types. Another 12% (three respondents) reported using eight strategies for data to drive sales.

Upselling and cross-selling was the most utilized application of customer data with 39% (of 26 respondents) reporting use of this strategy. Customer segmentation overall and by product was next at 36% utilization.

As the importance of accelerated underwriting gains traction in the U.S. and abroad as a means to increase sales by processing applications faster and more efficiently, 32% of respondents reported having a strategy in this area. Interestingly, only 29% reported using underwriting data propensity models based on criteria such as smoking status, aggregate credit ratings, driving records, and behavioral history.

The use of additional data strategies with a customer focus can be found in Figure 7.

Figure 7:

Administration and Customer Marketing

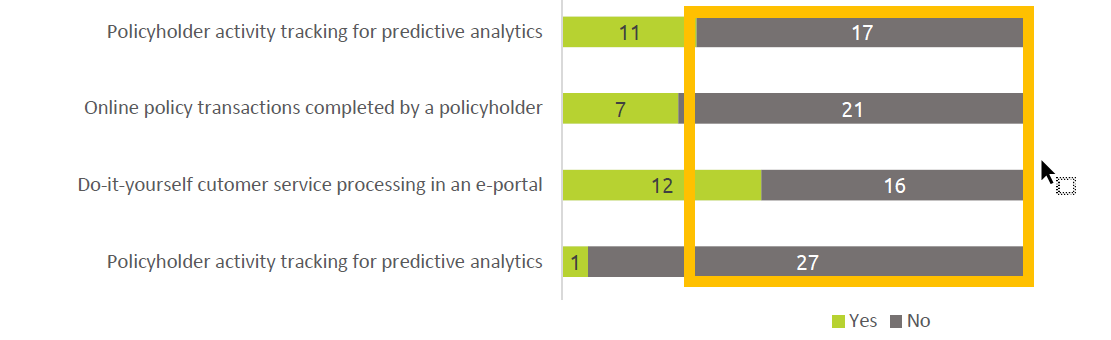

Administration capabilities lagged among survey respondents, indicating a potential opportunity to build on these capabilities for customer support. Eleven out of 28 reported having policy e-delivery (a PDF of the policy) option, while do-it-yourself customer service processing in an e-portal was indicated by 12 participants. The ability to perform online policy transactions by the policyholders yielded just seven affirmative responses. Lastly, only one respondent reported the capability to facilitate policyholder activity tracking for predictive analytics. Figure 8 highlights the results.

Figure 8:

Administration Capabilities

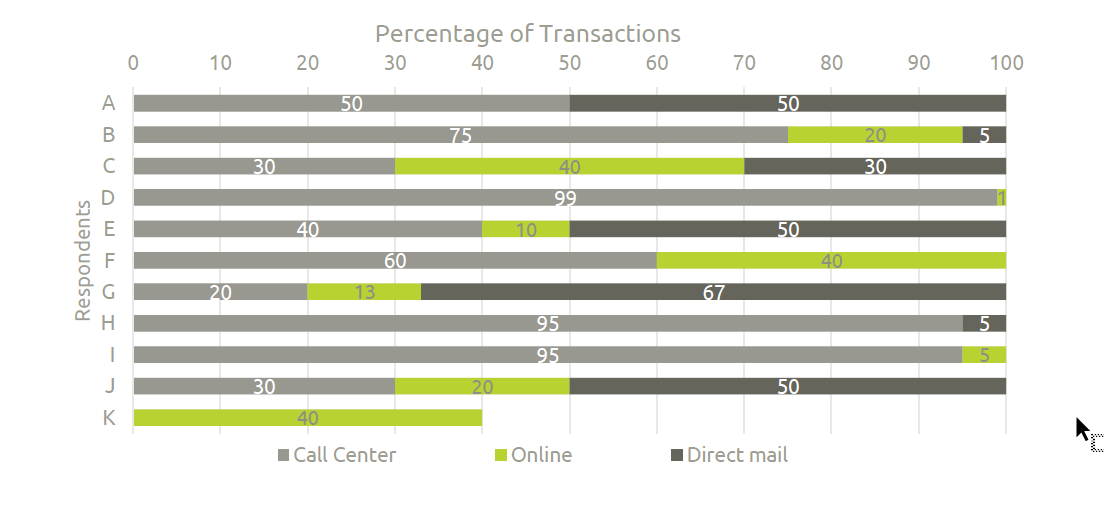

As illustrated in Figure 9, some respondents reported that online transactions make up as much as 40% of business. Generally, however, call center and direct mail channels still account for the majority of transactions.

Figure 9:

Customer Campaigns and Outreach

Figure 10:

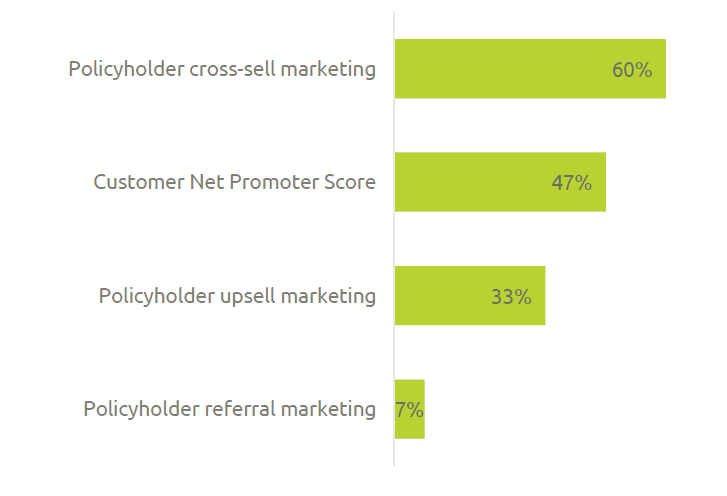

The customer campaigns indicated by 21 respondents included policyholder cross- sell marketing campaigns employed by 60%, followed by 47% that use customer net promoter score campaigns, and 38% for policy upsell marketing campaigns. Only 7% reported employing policyholder referral marketing.

Figure 11:

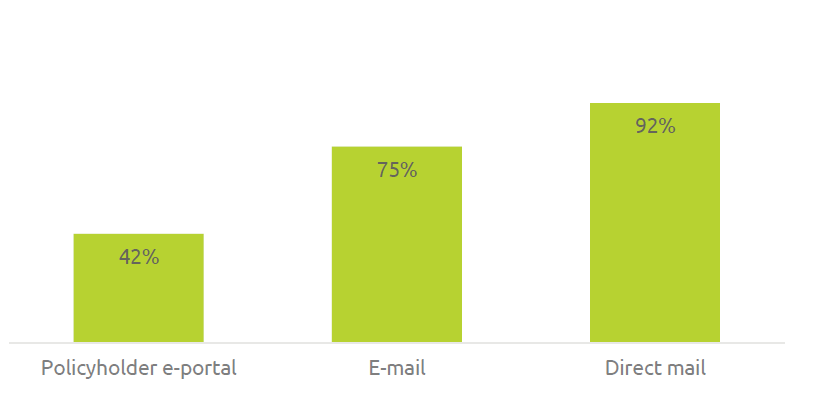

Outreach for customer campaigns (12 Respondents

The most popular method of outreach for customer campaigns indicated by 12 respondents was direct mail (92%), followed by e-mail (75%) and the policyholder e-portal (42%).

Customer Engagement and Loyalty Plans or Campaigns

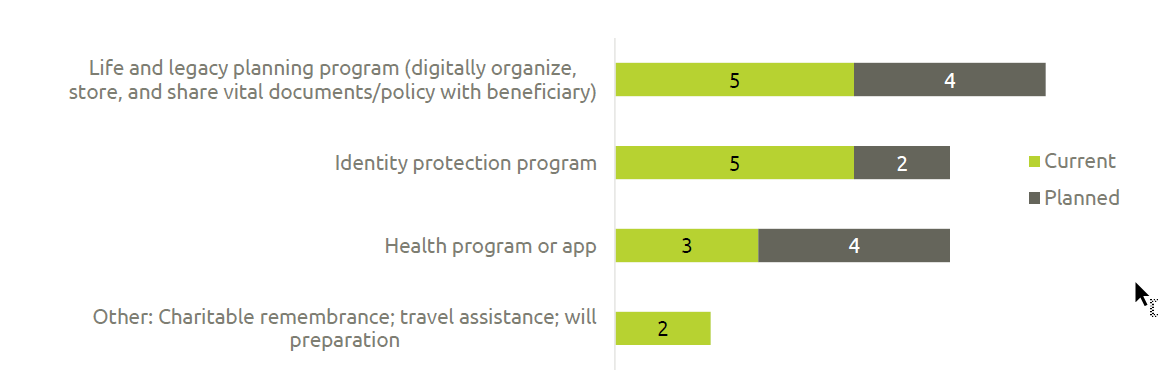

Thirteen survey respondents reported that they currently have engagement or loyalty plans in place, or are planning to implement these plans or campaigns in the future to increase customer engagement. As illustrated, below, in Figure 12, life and legacy planning programs are the most popular, with nine respondents having a program in place and four planning to implement one.

These programs allow customers to digitally organize, store, and share vital documents or policies with beneficiaries.

Identity protection programs were the second most popular response with five insurers reporting programs in place and another two that plan to offer it. Health programs or apps, such as tele-doctors, prescription discounts, and wellness check-ups, yielded three responses for current use and four for planned implementation.

Figure 12:

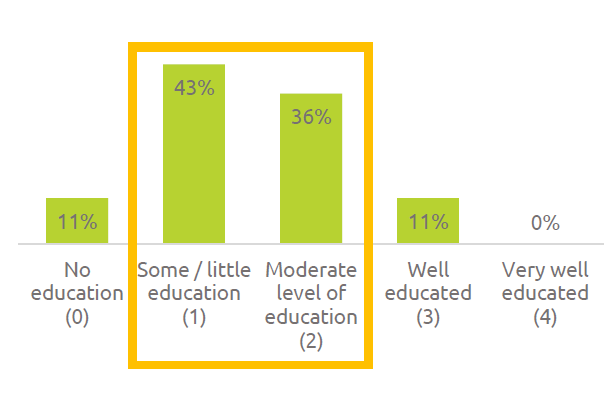

Education and Level of Insurer Digital Marketing Capabilities

Carriers were asked to evaluate their level of education on digital marketing capabilities. The majority of responses were concentrated around “some or little education” (43%) and “moderate level” of education (36%). See Figure 13 below. Interestingly, only 11% indicated either “no education” or “well educated” on digital marketing capabilities.

Figure 13:

Respondents' Level of Education on Digital Marketing Capabilities

Figure 14:

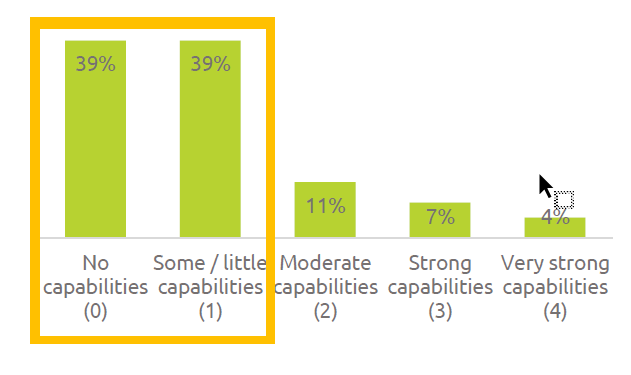

The level of capabilities for insurers varied drastically from the level of education. Predominantly insurers reported that they had “no capabilities” in the D2C channel or “some/little capabilities” thus far after having started testing digital marketing. The remainder of respondents cited moderate (11%), strong (7%), and very strong capabilities (4%).

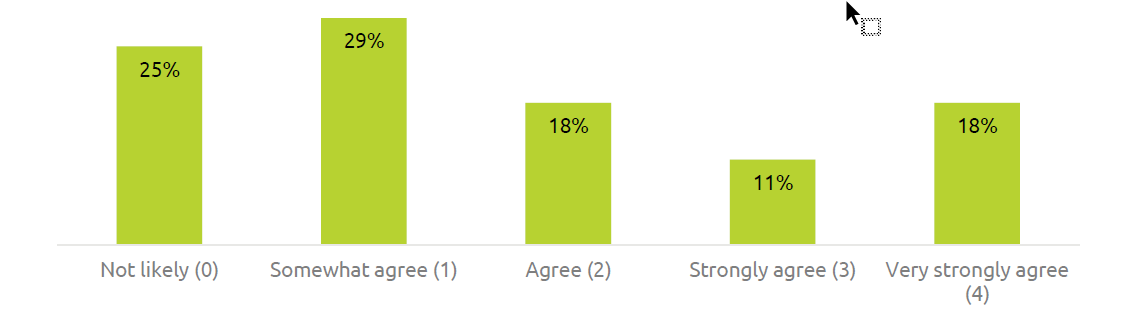

Expansion of D2C Distribution with Dedicated Digital Marketing Capabilities

Survey respondents who have started digital marketing in a D2C channel indicated their plans for expansion. The findings were very spread out with 25% reporting “not likely,” 29% “somewhat agree,” 18% “agree,” 11% “strongly agree,” and 18% “very strongly agree.” Please refer to Figure 15.

Figure 15:

We have dedicated digital marketing capabilities and will continue to expand on D2C distribution

For respondents indicating that they agree or very strongly agree, we noted that they have plans to grow strategically and planned allocation of resources (e.g., hired full-time staff and plan to engage the agents). One respondent reported the use of underwriting tools that base risk selection on algorithms. Those who “very strongly agree” to D2C distribution expansion cited beta testing in selected states and are making progress across the U.S. as they add products to the platform.

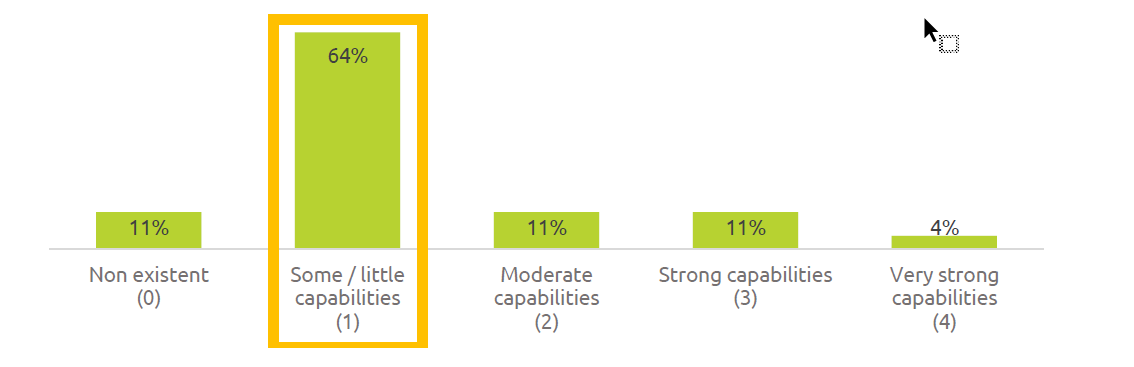

Expansion of D2C Distribution with Dedicated Digital Marketing Capabilities

When asked how they would rate their own overall digital marketing capabilities, the majority of companies (64%) indicated “some/little capabilities” (refer to Figure 16). Additionally, 11% respectively responded “nonexistent,” “moderate,” and “strong.” “Very strong” was recorded among a mere 4% of survey respondents.

Figure 16:

Digital Strategy Advice from Vendors and Partners

52% of 25 respondents surveyed have vendors or partners advising on their digital marketing strategy. The partnerships cited by respondents included advertising agencies, marketing firms, third-party consultants, research groups (e.g., LIMRA), and reinsurers. Additionally, insurers reported that they outsource to third parties and engage lead generation partners and other vendors with knowledge and technology to support their digital strategy.

The companies that responded they have “moderate” or “strong” capabilities stated that they partnered with several companies or outsourced much of their digital marketing.

Digital Marketing Resources

Figure 17:

Digital Marketing Resource

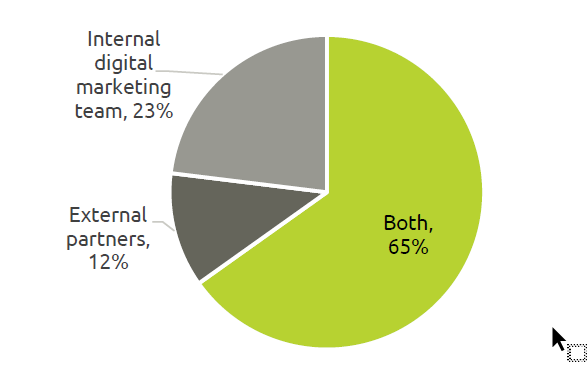

In terms of resources to support digital strategy, 23% of all respondents reported having an internal digital marketing team, while 12% work with external partners. The remainder, 65%, use both an internal digital marketing team and external partners.

Costs Associated with Digital Marketing Efforts

Survey findings indicate that 29% of respondents think it is too expensive to introduce or expand digital marketing efforts. However, several carriers elaborated on this topic and revealed that while they don’t believe it is necessarily too expensive, investment in digital marketing is not yet a recoverable cost – but could be if executed correctly. Three highlighted insights are captured here:

“Not too expensive, but the spend needs to be based upon anticipated ROI and additional leverage points contemplated in future business.”

“Digital marketing efforts take a culture shift and sea change that requires investment in time and money. Digital marketing would need to be prioritized with other investments in the portfolio.”

“We continue to find more inexpensive ways, but currently the external vendors we have talked to are really out of our price range.”

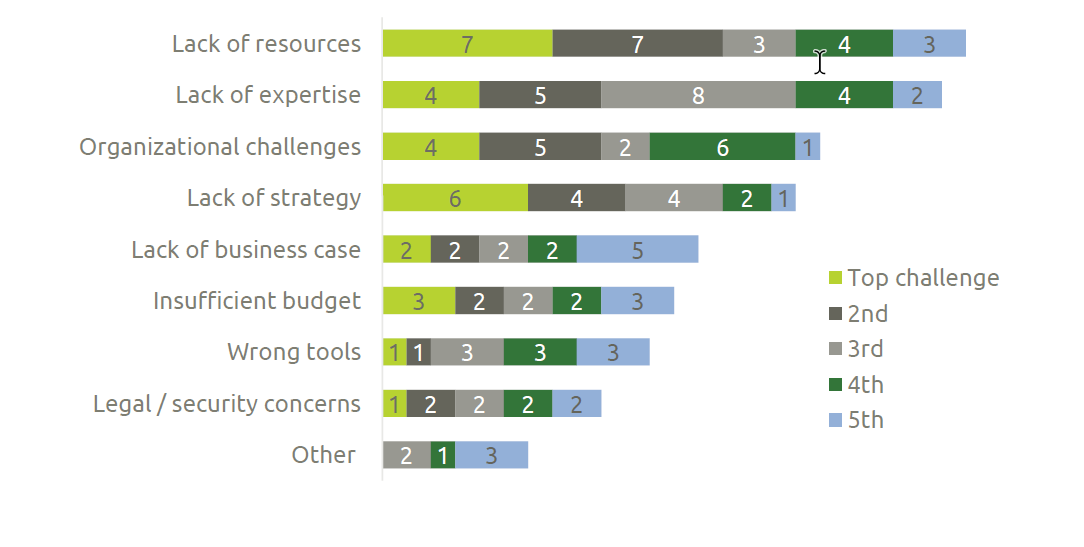

Challenges to Incorporate Digital Marketing to Improve Customer Experience

The biggest challenges that organizations face when trying to incorporate digital marketing to improve customer service (listed by number of respondents rating each a top-five challenge) include lack of resources (24), lack of expertise (23), organizational challenges (18), lack of strategy (17 – but six first-place votes), and lack of business case.

Figure 17:

Conclusion

RGAX’s “Digital Distribution Strategy Survey” of small-to-medium-sized U.S. insurers revealed that 64% of respondents rated themselves with “some or little” capabilities for overall digital marketing capabilities and 43% reported having “some or little” education.

The majority of carriers predominantly market fully underwritten term products, annuities, fully underwritten whole life, and universal life products. The concentration of distribution tended to be through independent agents, with the integration of digital marketing.

Advertising, D2C websites, online quoting, and risk selection scoring are the digital marketing areas that are currently enabled, are being expanded or built out in 2018, or are planned for implementation within the next three years. Carriers continue to partner with startups, insurtechs, and other third parties for further development of D2C channels, accelerated underwriting platforms, and mobile delivery options to increase customer satisfaction.

The use of strategies to leverage data is an area for improvement, with less than half of respondents using customer data for upselling and cross-selling, models for accelerated underwriting, or customer segmentation. Another area of development is administration capabilities, including policy e-delivery, do-it-yourself service processing (in an e-portal), and online policy transactions completed by a policyholder.

Engagement and loyalty programs represent a growing opportunity, with the majority of respondents implementing life and legacy planning programs, identity protection programs, and/or health programs and apps.

While the cost of allocating resources and the expense of introducing/expanding digital marketing efforts remains high, many survey participants still felt that it is worthwhile and may be a recoverable cost, if done correctly.

The largest challenges to implementing a digital marketing capability to improve customer experience are: lack of resources and expertise, followed by organizational challenges and a lack of strategy. 52% of respondents reported partnering or using vendors to advise them on their digital marketing strategy. These partners or vendors included advertising agencies, marketing firms, consultants, reinsurers, lead generation partners, and tech vendors.

It is our hope with emerging tools, technology, and data-driven analytics, we can make the digital marketing space a bit more accessible for U.S. carriers and produce a better customer experience for consumers.