The purpose of this two-part article is to look at biomarkers (with a focus on NT-proBNP) in use or under investigation in the medical world that are not currently widely used in the insurance market.

We look at how we might use them in risk assessment methods, with an aim to improve experience, pricing and profitability. Consideration is given to how biomarkers can be used in the insurance environment, the problems in using these biomarkers, NT-proBNP versus the stress ECG and mortality and morbidity statistics.

Introduction

According to the American Cancer Society, the five-year relative cancer survival rates have risen from 55% in 1987-89 to 68% in the period 2003-09. Specifically, leukemia, myeloma, prostate cancer and NHL overall survival have improved by more than 15%1; however, ischemic heart disease, stroke and COPD remain the leading causes of death worldwide. The average life expectancy in 2012 of the global population was 70 years of age, up six years from 1990; the U.S. has added four years to its average age at death from 75 to 79, China is up from 69 to 75, the U.K. 76 to 81 and India 58 to 66 years of age12.

Discoveries in gene sequencing and enhanced diagnostic tools have pushed us into a new world of biomarkers and screening tests for a myriad of commonplace diseases. Biomarkers are indicators for processes that are involved in disease development and can be used for diagnosis, as an indicator of disease progression or to influence methods of treatment and management of disease. The insurance industry has already been using PSA as a screening tool for some time but there are still inherent problems in its application, since values can be raised for reasons other than prostate cancer. Any new test must be used in the appropriate context and the quality of the research data considered before implementing its use. As NT-proBNP is not used in clinical practice for screening purposes, the insurance industry is presented with a dilemma in how the biomarker should be used at the underwriting stage. For insurance purposes, we also need to consider the introduction of any new tests and the impact on the client, with the overall cost to the business.

Over-screening can lead to unnecessary worry, investigations and cost at the expense of business. The tests performed on clients should actually add value to the underwriting process and contribute to the overall profitability of the business. Our job is not to diagnose disease but to measure risk exposure of death or disease and to protect the book of underwriting business from undue losses. How we do this is defined by each company’s underwriting philosophy and stance in relation to screening tools. 45% of U.S. insurers were believed to be using NT-proBNP as a screening test in 20116, rising to 60% in 20137 and it is increasingly being used around the world in place of the stress ECG.

What is NT-proBNP?

Two forms of BNP circulate in the plasma, BNP-32 and the inactive pro-hormone N terminal fragment BNP (NT-proBNP). NT-proBNP is a peptide hormone discovered more than 20 years ago, which is produced in the ventricles in response to an increase in heart wall stress due to ventricular pressure and volume overload, hypertrophy and ischemia. While NT-proBNP is not associated with high blood pressure, it has been shown to be associated with arterial stiffness and is a predictor of an increased risk of atrial fibrillation as well as a marker for the presence of hypertrophic cardiomyopathy. It may also add value in the progression in renal disease, systemic lupus and ankylosing spondylitis. This biomarker separates all CHF and non-CHF patients with 90% sensitivity8. NT-proBNP is now used in the diagnosis and treatment of heart failure and is an accepted clinical practice. It may also be a valid marker for asymptomatic late cardiac damage and left ventricular dysfunction in persons treated with cardiotoxic (anthracycline therapy) chemotherapy and chest-area radiotherapy for cancer6. The test is not used in clinical practice as a routine cardiovascular screening test but we are seeing it being used by some insurance companies to help fine-tune their risk stratification. test is not used in clinical practice as a routine cardiovascular screening test but we are seeing it being used by some insurance companies to help fine-tune their risk stratification.

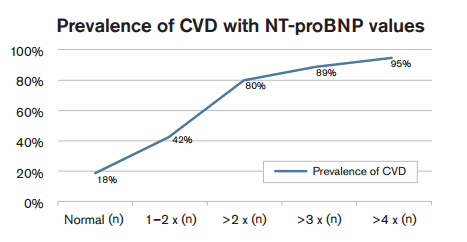

Mortality and Morbidity associated with elevated NT-proBNP*

Various studies have been carried out over the years, examining risk of death and probability of heart failure. Of these, the most prominent ones are examined below. It is clear that NT-proBNP adds value when looking at it from an underwriting perspective, but the problem lies in how to interpret the result and use the value in deciding on the application of any extra morbidity and mortality rate.

- The Framingham offspring showed increasing levels of BNP and NT-proBNP above the 80th percentile were associated with increased risk of death of 62% and 76% respectively and a three and five times risk of heart failure8.

- A nine-year follow-up study by the Mayo clinic of 2042 persons showed that NT-proBNP was independently predictive of mortality and heart failure in the general population free of CHF9.

- In a study by Clark, Kaufman and the Clinical Reference Laboratory, male mortality doubled where NT-proBNP range was 101-300 and up to 2.5 times in the >300 band in all sexes6.

- The Heart and Soul study Kaplan-Meier estimates of survival showed a progressive decrease in survival from the first (<64) to the fourth (>455) quartile8.

- The PREVEND study found that each doubling of NT-proBNP is associated with an increased risk of cardiovascular and all-cause mortality by 1.4613.

- The ADHERE study of 48,000 patients indicated that NT-proBNP had prognostic mortality values of 430 and above11.

- The Northwick Park Hospital study showed that a normal NT-proBNP virtually excluded several major cardiovascular diseases. The negative predictive value was 99% in ruling out AF, VHD or significant LVSD, and 96% in ruling out DHF (diastolic heart failure) although it was less effective in ruling out Left Ventricular Hypertrophy4.

Reference ranges and the problems with applying them at underwriting

It has been indicated that risk increases significantly above 300pg/mL in men and 200pg/mL in women, taking into account age, smoker status and other CAD factors3. While there is an increase in morbidity and mortality as NT-proBNP rises, there is no clear cut-off point in rising levels. There are several factors that lead to variances in recorded values:

- NT-proBNP may be higher in females due to the lower hemoglobin concentration or due to age-related fibrosis and subtle diastolic dysfunction4.

- At age 50 and above there is value in using it as a screening tool, but gender must be taken into consideration when looking at cut-off values3.

- It is important to consider BMI, as NT-proBNP levels are lower in obese individuals.

- Smokers were found to have a mean NT-proBNP twice as high as non-smokers in one study but this has not been found to be true across all studies5.

- NT-proBNP readings are significantly higher in those with severe fibrosis and cirrhosis in liver disease as well as chronic Hepatitis A, B and liver cancer5 6.

- NT-proBNP has been found to be raised in marathon runners, long-distance cycling and maximal exercise but always normalizes within 72 hours of rest6.

- It is increased in women, African Americans and Hispanic subjects, in menopause and often raised in anemia11.

- A study by the Department of Cardiovascular medicine in Northwick Park Hospital, U.K. of 2320 subjects > 45 years old found the following cut-off values: 100pg/mL for men aged 45-59 and 172pg/mL for men aged 60+ 164pg/mL for women aged 45-59 and 225pg/mL for women aged 60+

- Subjects with raised NT-proBNP had significant cardiovascular disease6

NT-proBNP versus the stress ECG

The stress ECG evaluates exercise capacity and any subsequent exertion symptoms such as dyspnea and fatigue. A normal stress ECG excludes a diagnosis of symptomatic heart failure10; however, it is a poor tool in the assessment of LV dysfunction, whereas NT-proBNP is a well-established base for this and is a valuable marker in decreased LV 2. As with any underwriting test or procedure, we need to consider both the hard and soft cost associated with the addition of any new underwriting requirement. NT-proBNP test is relatively inexpensive, costing about $40 per test, a much less costly option than a stress ECG test. The soft cost is associated with postponing cases that are otherwise healthy, with a risk of upsetting the client and/or agent and potential loss of good business. Problems arise in underwriting if a test or biomarker has low sensitivity/ specificity and is not very predictive of all-cause mortality.

- NT-proBNP may be advantageous over stress ECG where the stress test only reflects total plaque burden and is not influenced by unstable atheromatous lesions5.

- NT-proBNP test is simple to carry out as a routine blood test and is inexpensive.

- NT-proBNP may also be helpful in assessing cases of aortic stenosis and mitral regurgitation when results of recent echocardiograms are unavailable13.

- Oudejans et al. showed that NT-proBNP >440 had the same sensitivity as a resting ECG but twice the specificity in subjects with heart failure6.

- NT-proBNP may also be helpful in assessing cases of aortic stenosis and mitral regurgitation when results of recent echocardiograms are unavailable13.

- The City General Hospital, Copenhagen study showed levels of NT-proBNP increase with rising age and NT-proBNP increases with decreasing LVEF (p <0.050). NT-proBNP > 357 pmol/l (97pg/mL) identified those with an LVEF of < 40% (sensitivity 73%, specificity 82%) and the NPV below this value was 98%2.

Conclusions

While there is an associated increase in morbidity and mortality as NT-proBNP rises, there is no clear cut-off point in rising levels and here lies a dilemma in how to apply extra rates in underwriting. While NT-proBNP is already being used as a useful screening tool in place of the stress ECG in some markets, consideration should also be given to the benefits of using it as an enhancement tool to better define morbidity or mortality risk in different age categories or product ranges. Further thought could be given in using new biomarkers from an underwriting, or even in claims perspective, and more questions need to be asked as to what we are actually losing or gaining over existing screening methods and the impact on overall business. Using new biomarkers in the correct context could offer greater flexibility, faster turnaround times and speedier decisions, improved underwriting terms, reduce costs of screening and improve experience by more accurately defining risk, providing an opportunity for increased business volume.

Many of the current screening tests used in insurance focus on cardiovascular disease; the reality is that a higher proportion of claims in some product lines come from cancer related disease and as an industry we need to think about any imbalance in screening methods. The use of evolving biomarkers may have a place in the future of applicants applying for cover, particularly for cancer survivors and those with a history of chemo-radiotherapy. This is an area still under development and research continues into defining the protective value of these biomarkers.