Technological advancements in the last decade have tremendous potential to dramatically change personal wellness, healthcare, and insurance.

The development of new medical technology and smartphone applications (apps) related to healthcare creates an unprecedented opportunity to improve quality of life and longevity. Individual patients now have tools to understand and better manage their own health, and doctors are able to use new technology to more effectively treat patients. However, the effectiveness of the technology depends on the accuracy of the tools. Additionally, the greatest potential for improved healthcare results from technology supplementing traditional care, rather than replacing physician consultation. Used correctly, technological medical advances have the potential to improve treatments for patients as well as the transition from population-based to individualized care.

Consumers have the ability to utilize this technology to better understand their individual risk profiles and base insurance decisions upon knowledge that may not be known to insurers. This creates a significant risk to the insurance industry. However, these advances also have the potential to create opportunities for insurers as well. New medical technology can streamline the underwriting process and increase the market potential for insurers. Additionally, the opportunity for better health outcomes from technology aligns with the needs of individuals and insurers for people to live longer and healthier lives.

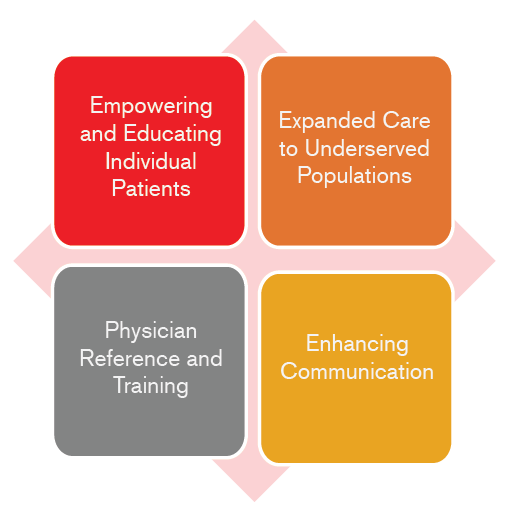

New technologies are being deployed to achieve a variety of goals:

Patient Education and Empowerment: Smartphones are a ubiquitous part of everyday American life. As a result, individuals now have the tools to access medical knowledge to research conditions and treatments. Devices are available to track virtually every aspect of their health and well-being.

Expanded Care Options: The proliferation of tools means that consumers may now be able to diagnose illnesses and diseases independently of a physician. Under-served populations may now access care with portable and remote technologies. The advancements of the last decade mean that healthcare is now available to many individuals who previously lacked access to quality healthcare.

Communication: This democratization of medicine means that patient interaction with the medical community is changing. In-person appointments are no longer the only way to receive care. The device that began as a method of communication, the cell phone, has created new and effective ways for patients and doctors to communicate.

Physician Training: Technological advances and predictive analytics have increased the accuracy of diagnostic tools and accessibility to medical literature. Doctors can now reference the cumulative knowledge of the medical community with the convenience of a smartphone application or wearable hands-free computer like Google Glass.

Empowering Individual Patients

People have been using technology for years to become better informed about their health. Patients will often request a specific medicine based on a television commercial. Similarly, websites such as WebMD have been providing medical reference to concerned patients for years. However, with the proliferation of smartphone technology and super-computing power from consolidated data sources, patients have increased options to educate themselves about their medical conditions.

The website MEDgle allows patients to enter symptoms, diagnoses, drugs, procedures or physicians into a probabilistic database to inform the patient about their medical situation. [1] There are also many apps available to educate patients, such as HealthTap [2] and the American Red Cross First Aid app. [3] Patients now have many more tools readily available to become more informed about their own personal health and wellness.

Data gathered from this new technology has led to a movement called the “quantified self”. [4] People now have the ability to study patterns in their own personal data.

Consumers can improve fitness and nutrition through a number of lifestyle gadgets and apps. Activity monitors such as Fitbit Flex, Jawbone Up, and Nike Fuelband track statistics such as number of steps, calories burned and even monitor sleep. These devices can synch to nutritional databases such as MyFitnessPal and Loseit to give people a broader understanding of their diet and exercise patterns. Clearly, the efficacy of these tools depends on consistent and accurate usage. However, with more than 35% of Americans defined as obese [5], these tools have the potential to improve the health of many people who are at risk for obesity-related illnesses. Individuals now have the ability to monitor health and actively participate in care. Medical device attachments to smartphones are available to monitor heart function [6] and take blood pressure. [7] Patients with heart diseases can regularly monitor heart rate, heart variability, blood oxygen, and respiration. [8]

People can collect various wellness statistics using tools such as Microsoft’s HealthVault which will consolidate nutrition and fitness data with cholesterol and blood pressure. [9] Similarly, the LifeWatch phone is a health and wellness phone that monitors heart, glucose, diet, and exercise, as well as gives drug reminders.[10]

Those with diabetes can keep better control of their blood sugar with blood glucose monitors such as iBGStar [11], as well as the Glooko Diabetes Management Platform.[12]

Many conditions that would benefit from early detection of symptoms and tracking have the potential to have improved outcomes using technology. For example, parents of children with epilepsy can use a seizure monitoring device that will alert the parent to a seizure and will also track symptoms to communicate with their physician. [13] Another example is an app developed to track and monitor symptoms of Bipolar disorder. [14]

Consumers not only have the ability to monitor and track their health; individuals are increasingly able to use technology to diagnose and test for disease and illness. The uChek iphone app is designed to perform a urinalysis at home. This device is able to identify abnormalities in urine to better monitor diseases such as diabetes and kidney problems as well as detect certain cancers and urinary tract infections. [15] The device is currently available for purchase in the United States but has not yet gained FDA approval. [16]

Many illnesses and diseases go undiagnosed for long periods when people do not have regular checkups or are embarrassed to test for certain diseases outside the privacy of their homes. Home testing, in lieu of a lab visit, is currently available in the United States for diseases such as HIV and hepatitis C, as well as cholesterol testing. [17] [18] A new device, the Measure from Mode Diagnostics Ltd, may gain FDA approval in 2014 to test for chlamydia, colon and prostate cancer, urinary tract infections, and drug use. [19]

Self-diagnosis carries significant risk if the test is inaccurate, resulting in delayed identification and treatment. There are several cell phone apps available that are designed to detect skin cancer based on digital images. The University of Pittsburgh tested the accuracy of these apps. The apps that give an automated response were found to give a false “Not Concerning” or “Benign” response to a cancerous lesion about 30% of the time. An app that had a physician review each image had much better accuracy. [20] This study emphasizes the potential risk from inaccurate diagnoses and the importance of continued oversight by a physician.

Although there are significant risks from inaccurate testing, there are also important potential benefits from individualized testing. In many cases, early detection can lead to earlier treatment and healthier outcomes. Consumers are able to use technology to identify signs of cancer in the early stages. An at-home test is currently available to test for blood in the stool, which could be an early sign of colon cancer. Additionally, there is a home Prostate Specific Antigen (PSA) test, to detect signs of prostate cancer. [17] A cancer detecting bra has been developed and is expected to gain FDA approval in early 2014. The bra is worn for a 12-hour period and is intended to detect breast cancer in younger women, for which a mammogram is less effective. [21]

Expanded Care to Under-served Populations

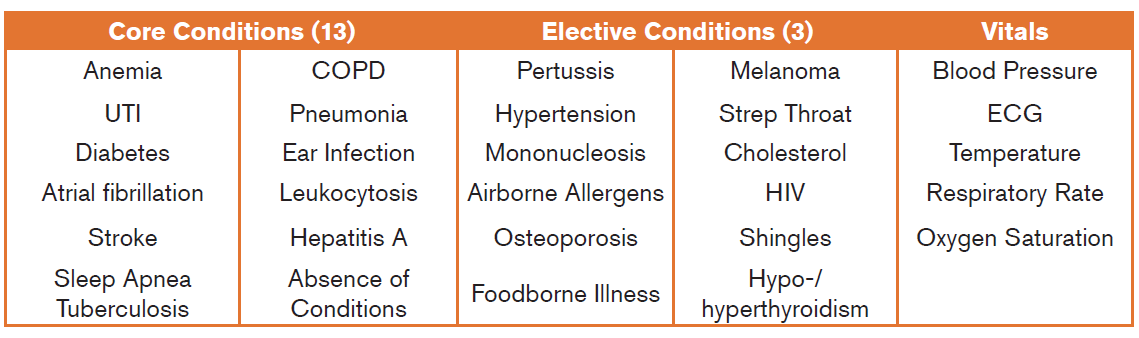

In 2012, Qualcomm introduced a $10 million “Tricorder Xprize”. The winner of the competition will be chosen mid-year 2015 and must accurately assess 16 conditions and five vital signs.

The motivation for this competition is to expand healthcare to underserved populations. Self-diagnosis will address the needs of the uninsured American population as well as reduce “ballooning” healthcare costs. Worldwide, many developing countries have significant shortages of healthcare workers. Enabling patients to self-diagnose will address some of the healthcare needs of these people.[22]

Since 2010, medical kiosks have become commonly installed in retail stores such as Walmart and CVS, with an estimated 2,500 installed by the middle of 2013. [23]These medical kiosks are equipped to perform basic vision testing, and take vitals and weight. Use of these kiosks is currently free. Therefore, people could use these kiosks to track and regularly monitor their health, resulting in improved health if people make use of the information. Also, if a person does not regularly see a physician, the data collected from the kiosks may be the only way they are able to find out potentially valuable information. However, if a person opts to forgo a more thorough evaluation with a physician due to the use of this kiosk there is a potential for relatively worse health as a result. As this technology becomes more prevalent, the implications for the health of Americans should become more apparent.

In 2013 the Tedmed conference highlighted apps that could be part of a “Smartphone Physical”. These apps include a digital stethoscope and scale, heart monitors, otoscope, and vision testing applications. [24] Smartphone technology has created significant opportunities to expand healthcare to underserved populations all over the world.

Vision and hearing loss are two of the top causes of disability in adults over 60, especially in low-income countries, according to the World Health Organization. [25]Many vision impairments are treatable, especially if detected early. There are cell phone apps available to identify and monitor vision impairments, such as “myvisiontrack”. [26] Additionally, hearing aids are unaffordable to many around the world, including the United States. A company called “Sound World Solutions” has developed a hearing product that is one-tenth the cost of traditional hearing aids. [27] Vision and hearing disabilities take years of life away from people worldwide; these apps have the potential of improving both the quantity and quality of life to many.

The World Health Organization estimates that more than half of the disease burden in low-income countries is due to communicable diseases. [28] The resolution in cell phone cameras has evolved to the point where communicable diseases such as malaria and tuberculosis as well as bacterial and parasitic diseases can be identified by remote doctors reviewing these images. [29] People living in areas of the world with few physicians and labs could benefit from this technology.

Enhancing Communication

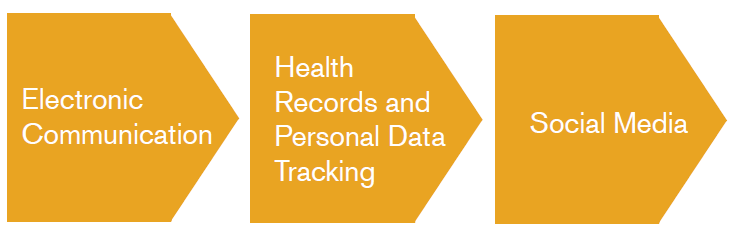

Patients are using new technology to find new ways to communicate with physicians without an office visit. A new app, PingMD, is designed to improve the efficiency of patient-doctor communication. Patients can send messages and videos to doctors to ask questions and see if a follow-up appointment is necessary. [30] Emergency services may become more efficient with a new 911 app to allow for more dynamic communication between emergency responders and people experiencing an emergency. [31] Similarly, the Medlert app attempts to streamline the emergency response system. The app has the user prefill information so the caller does not need to spend time on the phone giving background information. The emergency responder will have access to detailed information about the patient in a quicker manner and thus be better able to provide appropriate care. [32]

It is now possible for smartphone applications to augment health records. Discovery Health has developed a health record app that will allow physicians to review consolidated patient records electronically. [33] Additionally, patients can share data obtained from self-tracking apps. This gives doctors the ability to evaluate trends in data rather than rely only on snapshot data collected from in person visits. This data can become part of the consultation.

New technology has also evolved to better inform doctors about patient adherence to drug prescriptions. Smart pills have embedded sensors to alert doctors about patient use. [34] This has tremendous potential to improve care, especially for drugs that are highly sensitive to a strict schedule. Actual patient use of drugs can be monitored by doctors to prescribe the most appropriate medicine and dosage based on this usage data.

Technological advances are only a part of the reason for the shift in care from traditional distribution methods. An individual actively participating in their own healthcare is the main driver in the change in healthcare consumption. However, individuals working together have an even greater potential to shift standards of care. Social media can pool the knowledge of individuals to expand understanding of medical treatments; a good example of this is the website “CureTogether”. [35] Another example of the ability of social media to influence healthcare is an application on Facebook to facilitate matches between potential organ donors and recipients. [36] Similarly, DKMS, an organization also called Delete Blood Cancer, has set up kiosks in malls to facilitate bone marrow donor matches. [37] [38] Individuals equipped with technology can collaborate to change traditional medicine.

Physician Reference

Advancements in computing power have led to the expansion of analytics into hospital settings. In 2012, Memorial Sloan-Kettering Hospital announced a partnership with IBM’s Watson supercomputer to enhance cancer treatment. Watson’s natural language processing is capable of handling the complex nature of oncology as well as the vast amounts of medical research literature. Watson provides diagnostic and treatment recommendations based on evidence-based analytics. This means doctors can leverage statistically supported analysis to provide more informed care for their patients. [39]

Another new technology making inroads into medicine is Google Glass; several early adopters of Google Glass have been physicians. There are many uses for this new technology in healthcare. Physician training can benefit from hands-free access to computing capabilities. Complicated surgeries can utilize expert consultation. [40] Additionally, healthcare apps for Google glass have been developed, such as the app “CPRGlass” which provides instruction on CPR. [41]Many groups have aired privacy concerns regarding the use of Google Glass in healthcare. As this technology becomes more common, patient privacy will need to be directly addressed.

The portable computing power of smartphones provides endless reference and educational material for physicians and medical students. Technology has the potential to improve evidence-based healthcare as well as improve the efficiency of patient care.

Insurance Implications

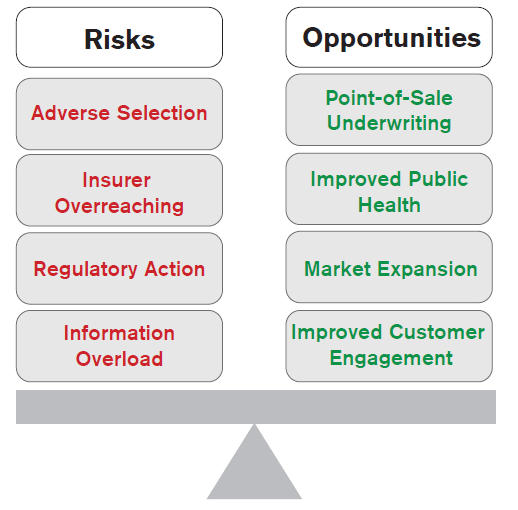

As personal health devices become smaller, cheaper, and more effective, insurers must recognize both the risks and opportunities this new technology creates. It is imperative that insurers understand the uses of new technology in order to effectively balance these challenges.

Risks

Adverse Selection

The insurance industry is characterized by a fundamental information asymmetry between consumers and insurance companies. Adverse selection is a by-product of asymmetric information as the demand for insurance is positively correlated with an individual consumer’s risk level. When insurers are not privy to the same information as consumers, they are not able to price the risk appropriately. Any disruptive technology that threatens to increase this asymmetry causes justifiable concern for actuaries, underwriters, risk managers and insurance companies.

Wearable technology, home diagnoses and many of the other technologies previously discussed create a potential “perfect storm” for adverse selection. The information that consumers gain from these technologies is generally:

- Low cost and therefore highly accessible

- Specific and therefore directly related to each individual’s risk profile

- Private and therefore not readily available to insurance companies

There are many examples of insurance products that demonstrate the link between information asymmetry and adverse selection. Simplified issue products generally have much higher mortality levels than similar fully-underwritten products, due not only to the value of the underwriting evidence but also to the anti-selective purchasing behavior on the part of applicants and agents. Level-term insurance has much higher mortality after the end of the level premium period due to the anti-selective lapse behavior of healthy insureds. Consumers with a genetic predisposition to Alzheimer’s disease have been shown to purchase long-term care insurance at a rate 5.76 times higher than those without such a predisposition. [42]

Insurer Overreaching

While there are many exciting opportunities to leverage the large volumes of data that is generated from new technologies, insurers must walk a fine line. On the one hand, data and technology may lead to products that are priced more accurately and sold in a less invasive manner, which should improve the customer experience. On the other hand, insurers must guard against misuse of personal data in order to preserve client trust. Any violations of that trust will undoubtedly have dramatic repercussions from a customer engagement, public relations, and regulatory standpoint. The focus of new technology must be on improving the customer experience and maintaining a fair balance of information between insurers and applicants. Treading too far, in the words of Hank George, is akin to “playing Russian roulette with our right to underwrite.” [43]

Regulatory Action

The accuracy of new medical technology is fundamental to the usefulness of the product. Insurers and consumers alike need assurance that the devices that are being used are safe and effective. Medical devices are regulated by the Food and Drug Administration (FDA), but the dramatic explosion of new technologies challenges the regulatory community to effectively regulate. Regulators have responded to safety and cyber-security concerns over device hacking of implanted devices such as pacemakers. [44] Additionally, the FDA intends to regulate products that are intended to diagnose or treat diseases, such as home urinalysis tests. [45]

Regulators have a variety of roles with respect to the use of new technologies in insurance. Globally there has been increased regulation around the security and privacy of personal health information, in recent years. Insurers must carefully navigate the U.S. requirements under the Fair Credit Reporting Act (FCRA), the Health Insurance Portability and Accountability Act (HIPAA),the Gramm-Leach-Bliley act, and related regulations along with a myriad of regulations in other jurisdictions to ensure that consumer data is being handled in a secure and appropriate manner.

Many jurisdictions have also moved toward increased restrictions to ensure nondiscrimination. In the European Union, the Gender Directive requires that rates must be equalized for males and females despite actuarially credible evidence that the underlying risk premia are different. A continuation of restricting the use of differentiating rating factors could inhibit insurers from utilizing much of the data collected from new technologies. If regulations further increase the information asymmetry between buyers and sellers of insurance, the insurance market will face an untenable future.

Information Overload

A practical reality of the expanding universe of information is the difficulty in analyzing the data to create a competitive advantage. This affects both consumers and insurance companies. Consumers may misinterpret the data from their “quantified selves” and forgo a visit to the doctor or make other poor health choices. Similarly, insurers may draw inappropriate conclusions from data due to sampling biases or model error. The biggest challenge for data scientists when analyzing large volumes of disparate data is separating out the relevant trends from the random blips: the “signal” from the “noise”.

Aggregating the data from the myriad of different device manufacturers and databases is an additional challenge. Currently, there are countless devices and applications for many individual ailments. However, the market does not have a dominant provider which is able to consolidate the information. Without a clear winner in this space, it becomes impossible to paint a complete picture of any one individual’s risk profile.

Insurers must also build the infrastructure and expertise to leverage the benefits of available data. This may create a disadvantage for smaller companies that lack the resources required to invest in enterprise-strength big data solutions.

Opportunities

Point-of-Sale Underwriting

The increased accessibility and mobile reach of medical devices create a unique opportunity for insurers to bring the underwriting decision closer to the applicant. Devices that are able to calculate physical measurements and effectively screen for the disease may reduce the need for standard paramedical exams and laboratory tests. By integrating the medical information collected at the point of sale with electronic application data, electronic underwriting evidence (MIB, prescription drug histories, motor vehicle records, criminal records, etc.), and ultimately electronic health records, insurers utilizing an automated underwriting rules engine or robust predictive model may be able to issue a policy in a fraction of the time of a typical new business process. In order for medical devices to streamline the underwriting process, it is vital to ensure a proper chain of custody of the evidence and technologies to maintain the high standards of sensitivity and specificity required to make an accurate and defensible risk assessment. Effective use of these technologies creates an opportunity to move the insurance purchasing process to a more transactional sales model.

Improved Public Health

Diseases associated with obesity and sedentary lifestyles have become increasingly prevalent and threaten to reverse a decades-long trend of increasing life expectancies. Consumers who modify behavior and lifestyle habits through use of the many fitness and nutrition apps may have improved health.

Medical technology can improve the quality of doctor appointments. These technologies enable improved monitoring of health statuses over longer durations, supplementing static data collected at periodic doctor appointments. Additionally, devices and apps can alert consumers to health conditions requiring consultation, prompting patients to visit a doctor in a more timely fashion. Earlier diagnoses and individualized treatments can potentially improve outcomes and lead to longer, healthier lives.

Life insurers and society alike will benefit through improvements in public health, expanded longevity and lower costs of chronic care.

Market Expansion

According to IBM research, the major focus of device manufacturers until recently has been at either end of the risk spectrum. [46] On the one side, you have what the Economist refers to as “an eclectic mix of early adopters, fitness freaks, technology evangelists [and] personal-development junkies.” [47] On the other side lie patients with chronic health conditions that require ongoing monitoring. The following graph demonstrates the continuum, and illustrates IBM’s contention that the largest untapped consumer segment lies in the middle among the “Information Seekers”.

Interestingly, the insurance underwriting process has been historically segmented in a similar way. On one end, companies have faced fierce competition for the best risks in their “super-preferred” underwriting classes. On the other end, underwriters have focused on screening out uninsurable or sub-standard risks. Again, the largest segment lies in the middle. Aligning the under-served consumer segments in the mobile health device markets and insurance markets can lead to an expansion in sales to both markets.

Improved Customer Engagement

Insurers and consumers have many aligned goals regarding health maintenance. Both want better health outcomes and a faster and less-invasive insurance purchasing experience. Through product, distribution, and underwriting process innovations that balance these mutual goals, life and health insurance companies can improve customer loyalty and persistency.

In the automobile insurance industry, companies including Aviva, State Farm, and Progressive have leveraged smartphone apps and telematics devices, such as Progressive’s “SnapShot”, to create a “pay as you drive” insurance premium based on a driver’s usage and risk profile. While the technology provides immense data upon which companies can build and refine predictive models of driving behavior, the most important feature of these technologies is the signaling effect. Information asymmetry is mitigated when the party with an information advantage is able to provide a verifiable signal to the other party that validates their trustworthiness.

Nobel Laureate George Akerlof famously analyzed the information asymmetry in the used car market. In order to narrow the information gap, sellers of used cars may signal to buyers by providing a vehicle history report, offering a warranty or allowing for an inspection. [48] Similarly, buyers of auto insurance can signal to the insurance company that they are safe drivers by volunteering to use a telematics device. Life and health insurers can utilize wearable technologies to create a similar opportunity for product discounts tied to the achievement of verifiable personal wellness goals.

Conclusion

The past decade has been a period of significant advancement in both technology and medicine. Individuals now have unprecedented capability to actively participate in their healthcare through monitoring, tracking and diagnosing many aspects of their health. At the same time, communication methods have changed to expand the ways in which patients interact with their physicians as well as other people interested in health and wellness.

The potential for improved health from technological advances is exciting, but these achievements provide both risks and opportunities for insurers. Any technology that increases asymmetric information increases the risk of adverse selection of consumers. Conversely, medical technology can be used by consumers to demonstrate health lifestyles. Understanding the challenges imposed by individualized quantified medical data is necessary for insurers to balance the risks and opportunities brought about by technological change.

For a deeper look at this topic, please see: Better Underwriting Decisions are Just a Heartbeat Away