RGA’s extensive research

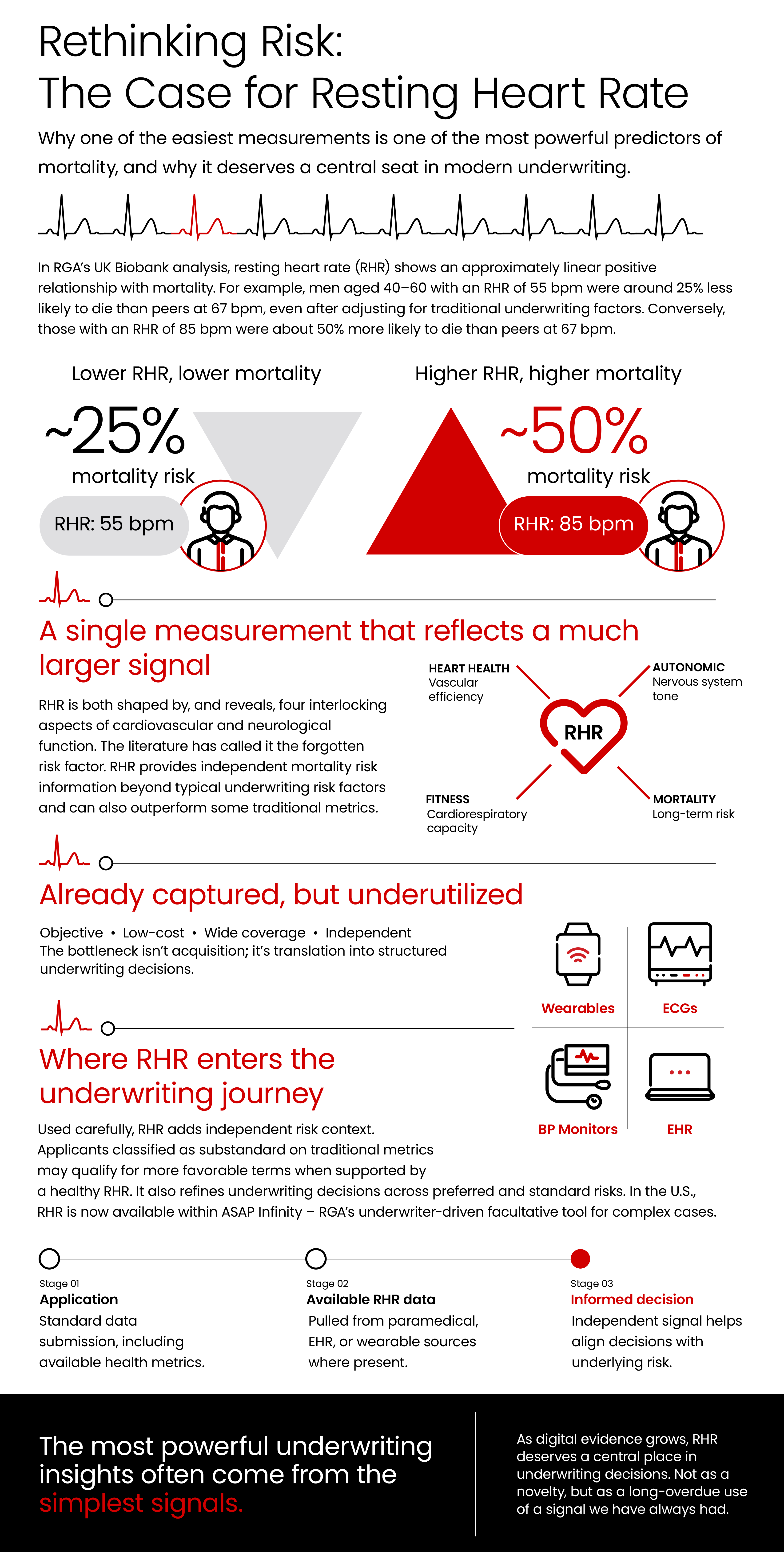

RGA’s broad research across multiple databases demonstrates that RHR is a robust predictor of all-cause mortality. For example, in RGA’s UK Biobank study, male individuals aged 40 to 60 years with an RHR of 85 bpm were roughly 50% more likely to die than peers with an RHR of 67 bpm, even after adjusting for traditional underwriting factors (Figure 1). While RHR measurements should be interpreted in context (e.g., medication use), RGA’s research shows that the relationship between RHR and all-cause mortality is remarkably consistent in different subpopulations. This predictive relationship holds across different age groups, both sexes, standard and substandard lives, and those with chronic diseases. Such consistency, across different populations, confirms RHR as an independent risk factor that adds incremental value to traditional underwriting metrics.

One of the most remarkable findings from RGA’s UK Biobank research is that RHR significantly outperforms total cholesterol as a mortality predictor. Similarly, RHR can replace BMI without meaningful loss of predictive accuracy. Some of RGA’s findings relating to RHR were published in a peer reviewed academic article with the University of Leicester in March 2026 in Mayo Clinic Proceedings: Innovations, Quality & Outcomes.10

Translating research into underwriting practice

As digital data sources become a routine part of underwriting, focus has increased on both identifying new metrics and making better use of the breadth of risk information already available to inform underwriting decisions. Within this context, RHR provides incremental risk information for underwriters. RGA is actively translating RHR research into underwriting practice. In the U.S., RHR is now available within ASAP Infinity – RGA’s underwriter driven facultative tool for complex cases.11,12 This helps bring evidence‑based insights into everyday underwriting judgments.

Figure 2 shows how RHR can be used as part of the underwriting process. For example, an applicant who might be classified as substandard based on traditional metrics may qualify for more favorable terms when supported by a healthy RHR. Similarly, RHR can be used to refine underwriting decisions across preferred and standard risks.

RGA is focusing implementation on facultative and preferred underwriting outside the U.S., while exploring other potential use cases. In this context, RHR offers a practical way to differentiate underwriting decisions, using meaningful evidence rather than unnecessary complexity.

Conclusion: Keeping fingers on the pulse

Underwriters should recognize the value of heartbeat metrics, particularly RHR. The growth of digital underwriting evidence, alongside advances in biosensors and wearable technology, means this information is increasingly available at the point of underwriting. As a result, guidelines must evolve to reflect the full breadth of relevant risk data now routinely available to underwriters.

The opportunity to improve underwriting accuracy using heart rate information is no longer theoretical. Making better use of this data can deepen understanding of individual risk, support more proportionate evidence requirements, and help ensure premiums remain aligned with underlying risk – creating benefits for both insurers and clients.

Contact us today to learn more about how to turn RGA’s biometric insight into results for your business.

psd.jpg?sfvrsn=12357542_1)