Life and Health Insurance Underwriting is entering a “new normal”.

The industry is moving beyond exploring new technologies, such as advanced data analytics and automation, to real-world applications. In this new environment, innovation is not seen as novel but as critical to the success of the insurance enterprise. Insurers are taking tangible steps to fundamentally change the ways that global life and health risks are underwritten.

When RGA last surveyed chief underwriters of large and multinational insurers in 2017, we discovered that insurers were being challenged to keep up with advances in underwriting technology and to lead the kind of business process transformation necessary for growth. In 2020, we find that companies are viewing transformation as business-as-usual and lining up significant investment to see that vision through.

Our 2020 survey, conducted online from December 2019 to February 2020, queried underwriting leaders from large global, regional, and single-market life and health insurance companies about their priorities and challenges in this radically changing climate.

Following the completion of this survey, the global COVID-19 pandemic disrupted strategies and new business processes for most, if not all, players in the industry. The survey explored topics such as “selling at a distance,” automating underwriting, and using digital/alternative evidence. These trends are more important than ever as insurers race to adapt to the new realities of selling insurance, for example, limited access to parameds.

If we were to conduct the survey again against the backdrop of the pandemic, we are confident that themes such as digitization and digital evidence inputs would score even higher than they did pre-pandemic. Globally, underwriting leaders seem to recognize that the pandemic may well prove to be the catalyst that drives the next wave of digital transformation in the industry.

When transformation becomes the priority

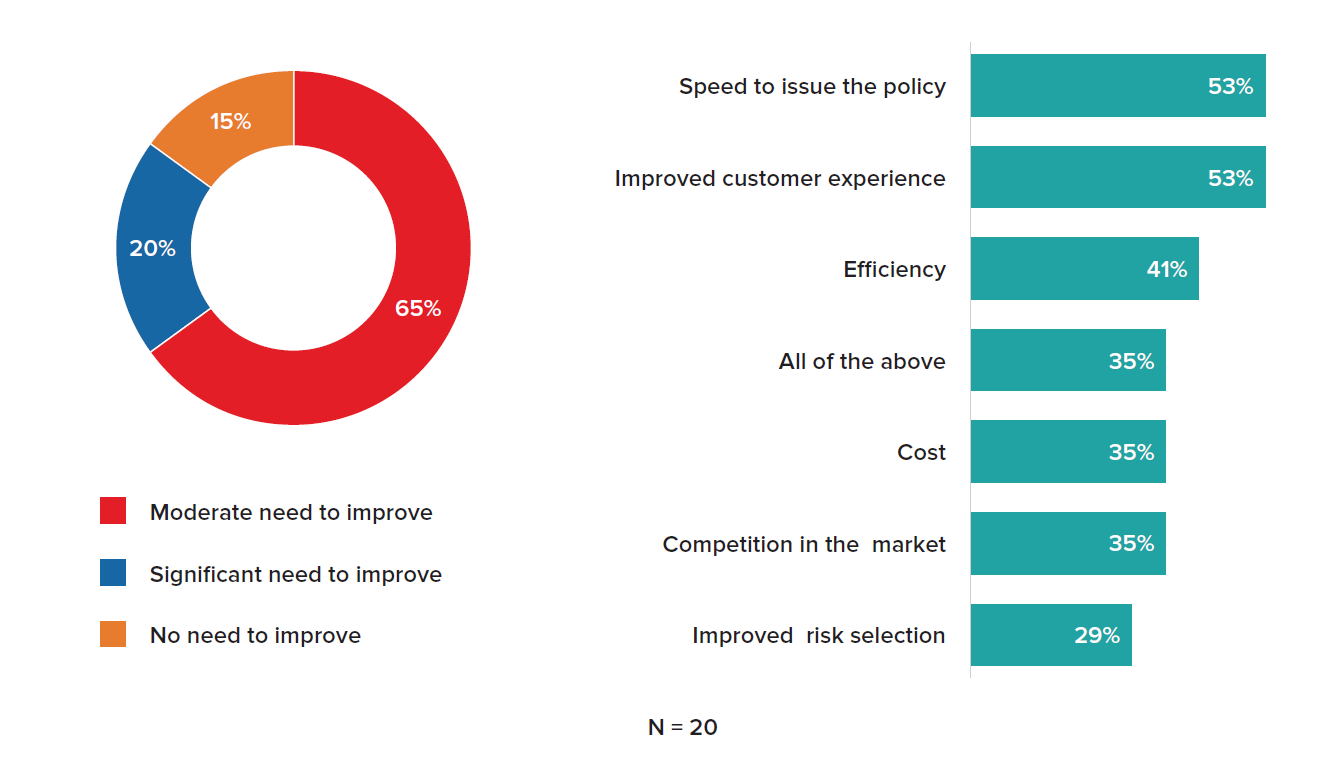

In our survey, the majority of underwriting leaders perceived a need to improve underwriting performance. Improvements in their underwriting performance was signaled by 85% of respondents with a moderate or significant need; the top areas of focus for improvement include enhancing the speed of policy issue (53%), improving the customer experience (53%), enhancing efficiency (41%), and reducing cost (35%). Consumer engagement, including speed to issue, remains the key focus for improvement efforts, with cost continuing to be a less important consideration. Interestingly, the number of insurers indicating a significant need to improve was 20% in 2019, down from 48% in 2017, suggesting that respondents had instigated continuous improvement and innovation initiatives since our last survey.

Figure 1:

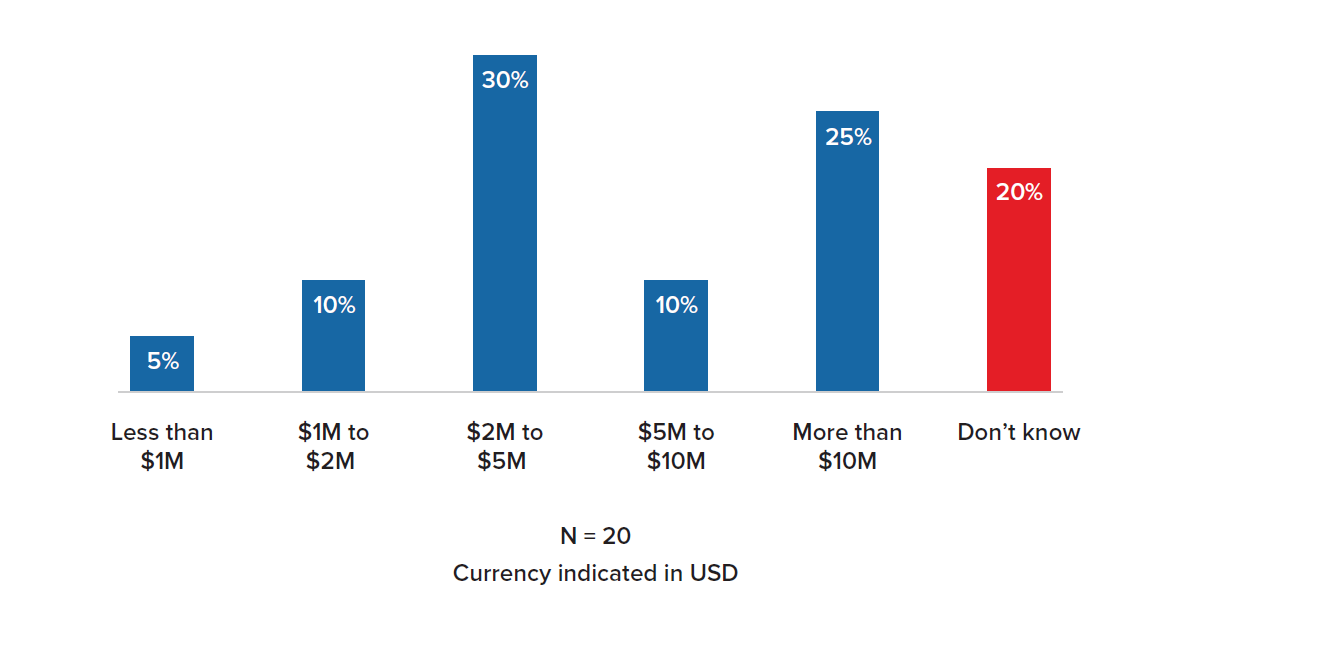

Survey findings reveal that change is underway, and respondents are committing to significant investments over the next 3-5 years to make gains. When it comes to commitment to underwriting transformation, insurers are eyeing larger expenditures: only three in 20 are investing less than $2 million over the coming 3-5 years to take advantage of new approaches. Investments of this size by larger players may put additional pressure on smaller insurers to invest in process change, even if this means adopting less substantial or incremental digital transformation solutions to remain relevant. Notably, RGA has recently seen an increase in demand for such light digital underwriting solutions when engaging with clients.

Figure 2:

Anticipated Expenditures on Underwriting Improvements in the Next 3-5 Years

Figure 3:

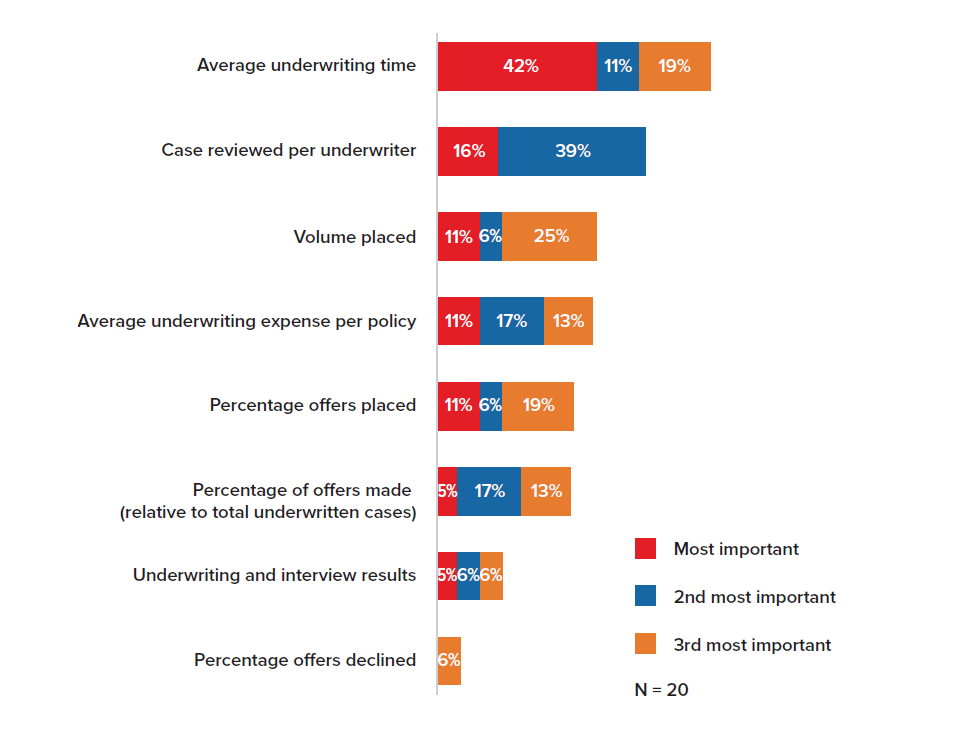

It is interesting to note that so much emphasis remains on turnaround time time since a more balanced approach includes placement as a key metric for measuring underwriting effectiveness and efficiency.

Drivers of underwriting innovation and disruption

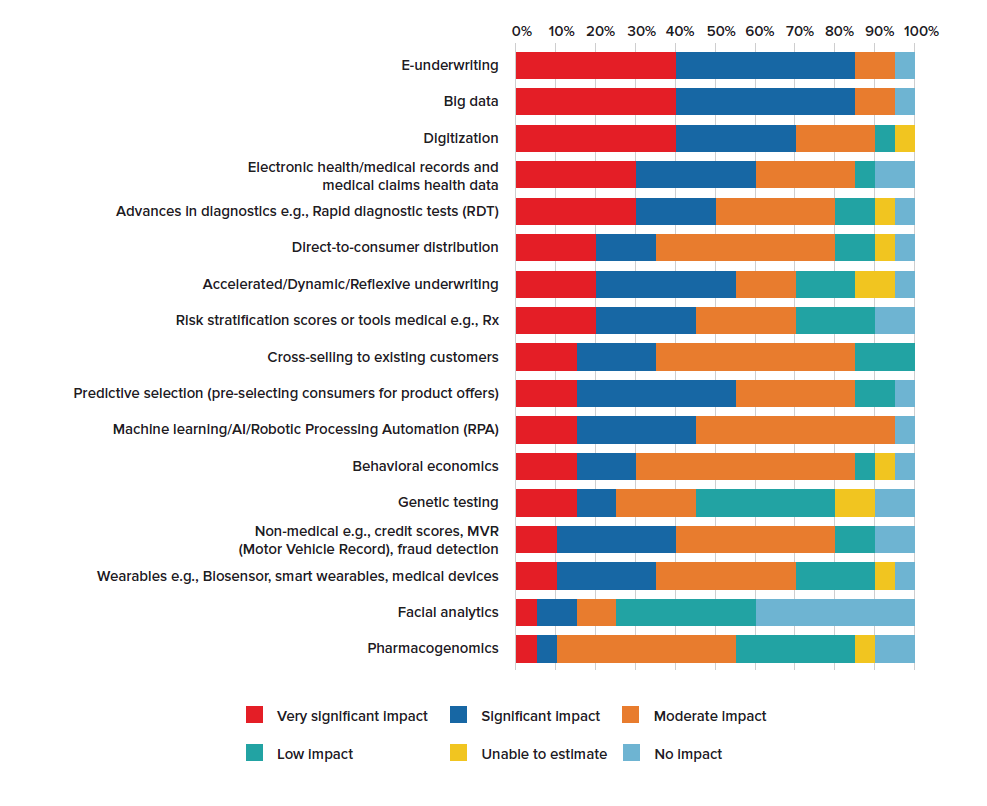

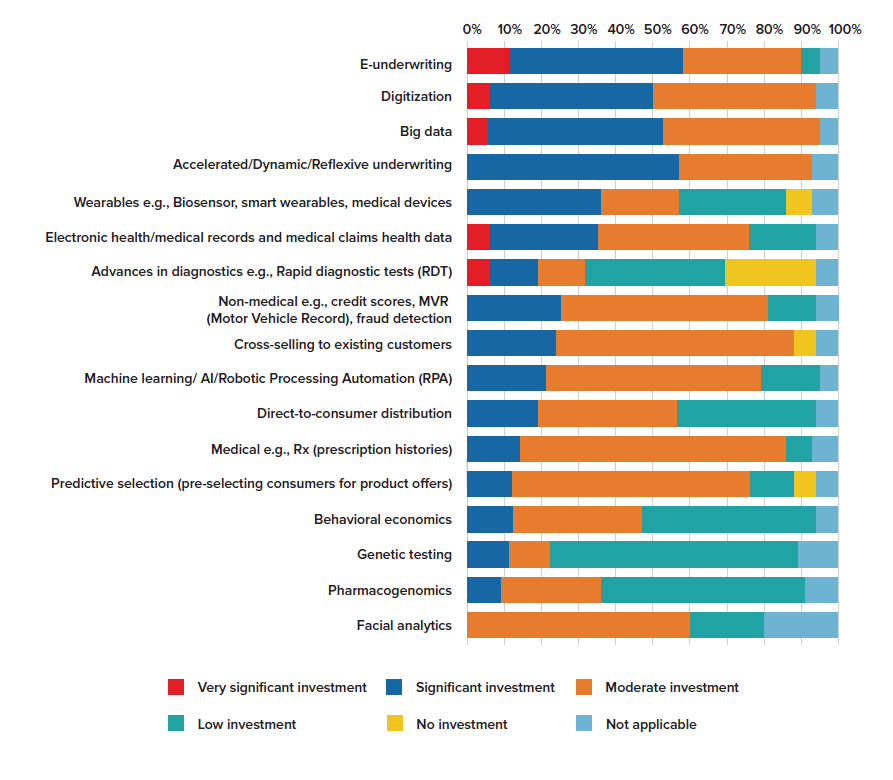

We asked underwriting leaders which innovations would have the most significant impact on the life and health underwriting function over the next three years. Automated or e-underwriting and big data topped the list, with 85% indicating a significant or very significant impact. Digitization (i.e., underwriting evidence in a structured digital format) finished next with 70% indicating the same potential impact. Electronic medical records were indicated by 60% of respondents, while accelerated/dynamic/reflexive underwriting and predictive selection (pre-selecting consumers for product offers) were indicated by 55%. As mentioned in the summary, demand for digitization and digital evidence can only increase in light of the unprecedented constraints imposed by the COVID pandemic. Lacking in-person access to prospective policyholders, insurers face the choice of selling at a distance or not making the sale.

Figure 4:

Expected Impact of Disruptive Innovations on the Underwriting Function

Interestingly, wearables were indicated by 35% of respondents, a slight upwards trajectory from 20% in the 2017 survey, while machine learning/AI/RPA was indicated by 45%, slightly down from 48% in 2017. Pharmacogenomics and facial analytics were ranked at the bottom of the list.

When it came to which disruptors insurers were investing in or planning on investing in, not surprisingly e-underwriting topped the list with 58% planning on investing significantly or very significantly. Only 20% of those surveyed indicated a plan to invest significantly in direct-to-consumer distribution – a number we would expect to see increase following worldwide social isolation orders and the resulting impacts to other distribution channels.

Figure 5:

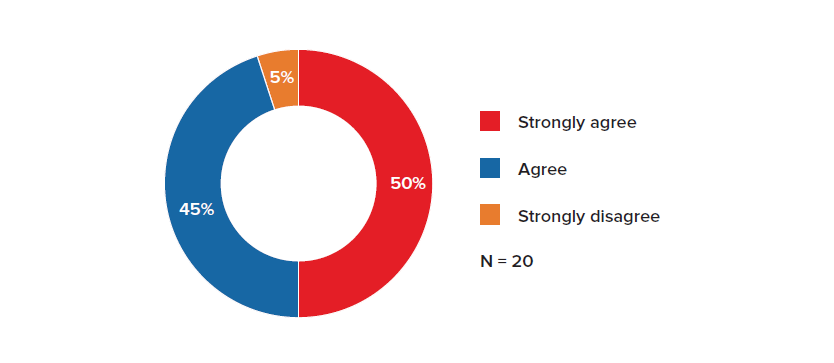

However, with the availability of new technologies comes disruption risk, particularly for entrenched or established players. When asked if new technologies and methodologies create opportunities, 95% agreed or strongly agreed that greater technical agility and freedom from legacy systems and processes could confer a competitive advantage to new entrants over more established insurers. This competitive pressure is clearly in the backdrop as new entrants seek to win market share by introducing novel, tech-enabled approaches. The impact of COVID-19 likely will push insurers to implement digital strategies within much shorter timelines to expand, or simply maintain, market share.

Figure 6:

New Technologies and Methodologies Create Opportunities for New Market Entrants

Improving the customer experience

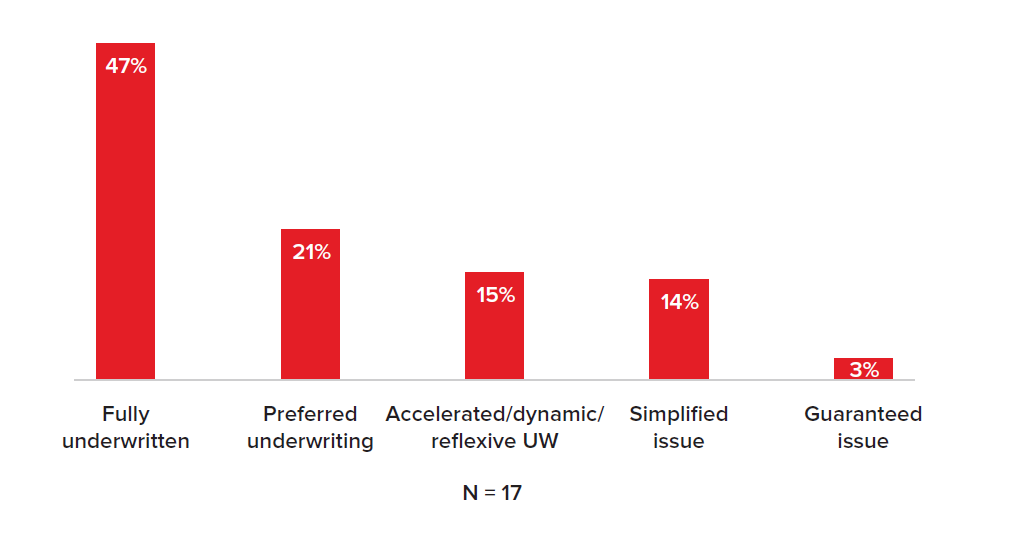

The fully underwritten process has been singled out as one of the largest consumer friction points in the customer journey. The emergence of the COVID pandemic has exposed significant weaknesses in the resilience of the fully underwritten model, as the ability to collect “face-to-face” underwriting requirements across multiple jurisdictions was constrained. In our survey, participants estimated that nearly half of all new business revenue came from fully underwritten approaches today.

Figure 7:

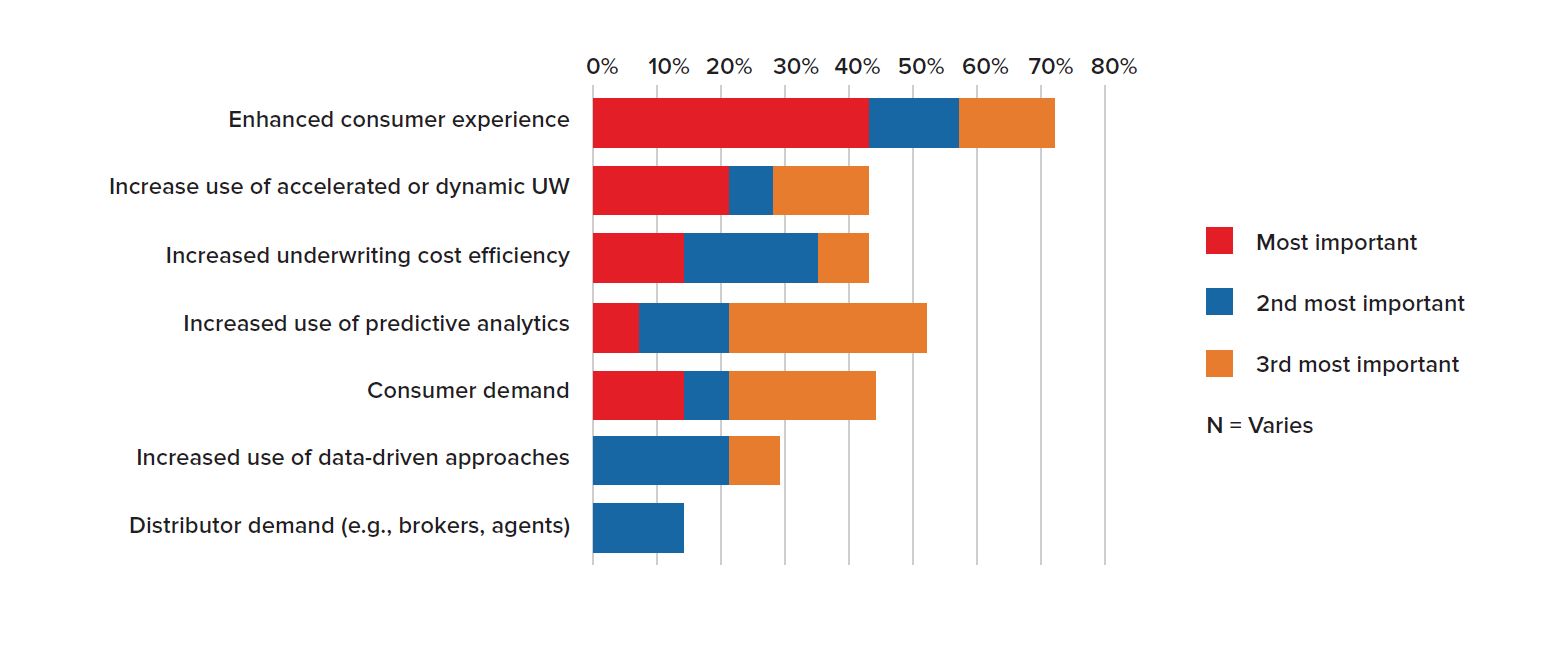

On a forward-looking basis, however, 65% of participants expect the percentage of new business that is fully underwritten to decrease over the next 3-5 years. Participants cited customer experience enhancement and the ability to increase use of predictive analytics as top factors driving the shift. Insurers are seeking alternative underwriting models that do not compromise mortality/morbidity outcomes. Rather than seeing fully underwritten approaches disappear, insurers are trying to replicate the same performance through alternative means, while achieving a better customer experience. For example, there is growing interest in the predictive power of credit data and digital health data.

It is no surprise that many respondents believe consumers are demanding modernization. Forty-five percent of respondents indicated that consumer demand was a top driver behind the transition to less invasive approaches to underwriting. This is consistent with results from the 2017 survey.

Figure 8:

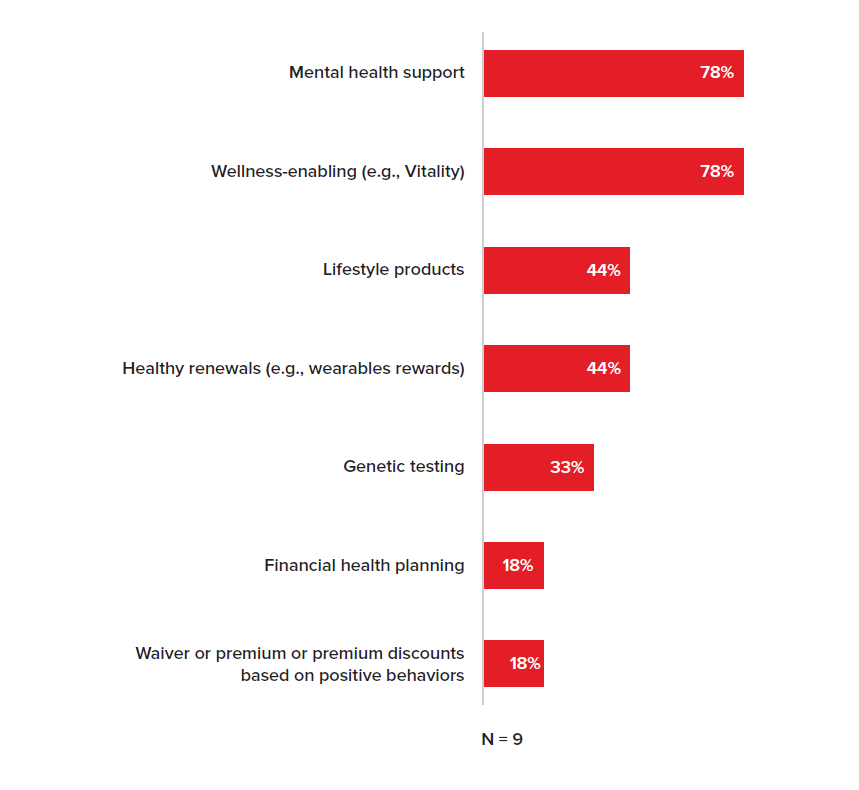

When it comes to enhancing or augmenting the consumer experience, our study showed that insurers are considering bundling more services alongside the insurance product to improve overall customer value. Forty-five percent of insurers surveyed indicated they were offering ancillary services to customers, with mental health support (78%), wellness (78%), and lifestyle products like gym memberships (44%) topping the list of services offered. It will be interesting to see if genetic testing becomes more important in the wake of COVID-19 as focus increases on the potential role of genetics in explaining susceptibility and immunity to the virus.

Figure 10:

Automated underwriting

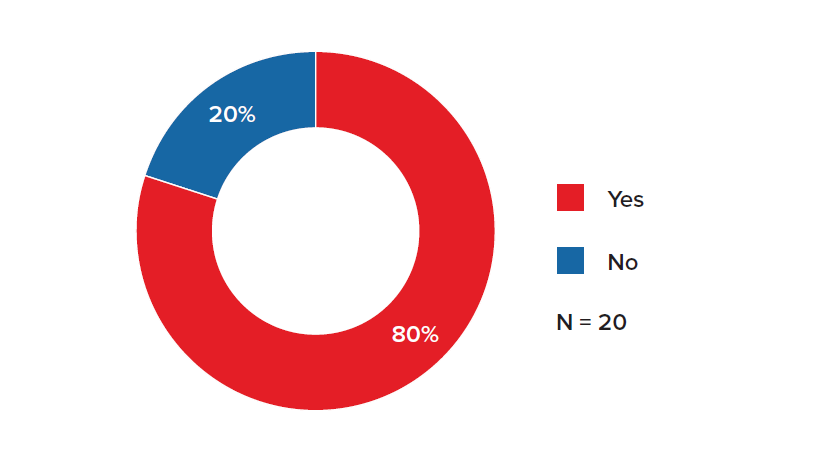

Automated underwriting has been a growing priority for life and health insurers for over a decade. In 2013, when RGA surveyed large and multinational insurers, 77% had deployed e-underwriting systems. Our latest survey reveals only slightly more – 80% of respondents – deployed these automated underwriting systems, suggesting that interest may be plateauing.

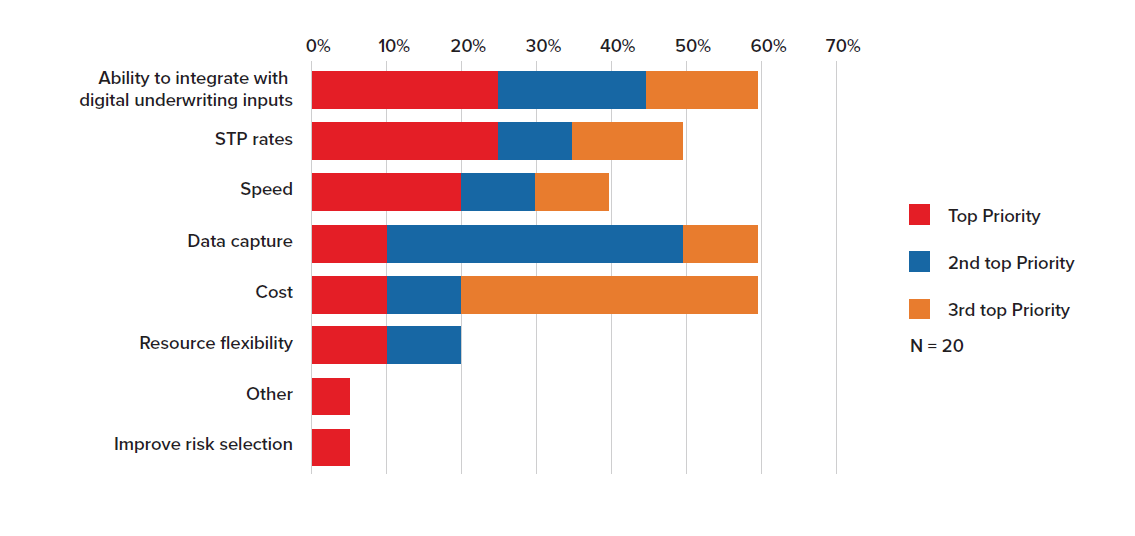

When asked what attributes of an e-underwriting system are most important to driving future growth, the ability to integrate with digital underwriting inputs, data capture, and cost were at the top of the list, with 60% seeing those as one of the top characteristics. These results contrasted with our 2017 survey results where Straight Through Processing (STP) rates were identified as the top driver.

Automatic underwriting continues to be the cornerstone that underpins any digitally underwritten offering. It is the heart of any program that incorporates risk assessment models such as credit or electronic health records. With so much of the future underwriting strategy relying on digitization of evidence and new risk scoring approaches, properly laying the automatic underwriting foundation is absolutely critical.

Figure 12:

Most Important Attributes of e-Underwriting Systems to Drive Future Growth

Use of data

Data-driven underwriting has long been the hot topic in life and health insurance, but survey participants report sluggish execution of data strategies. In many jurisdictions around the world, lack of access to proven predictive data sources, as well as supporting data infrastructures, has held the industry back.

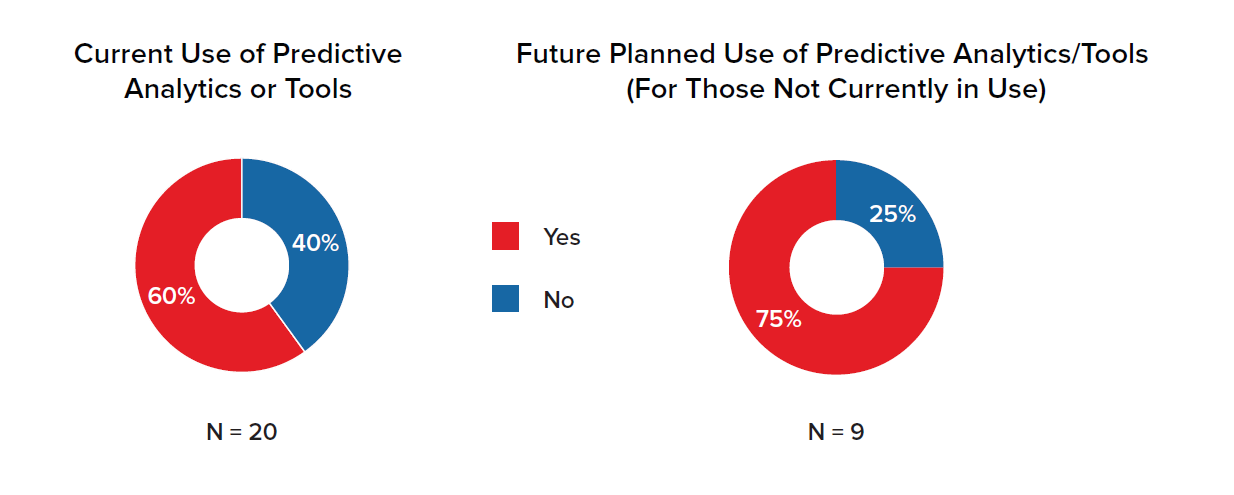

In our survey, 60% of respondents are using predictive analytics and tools in their underwriting processes. Of the remaining 40%, three-quarters expect to use predictive tools in the next 3-5 years.

Figure 13:

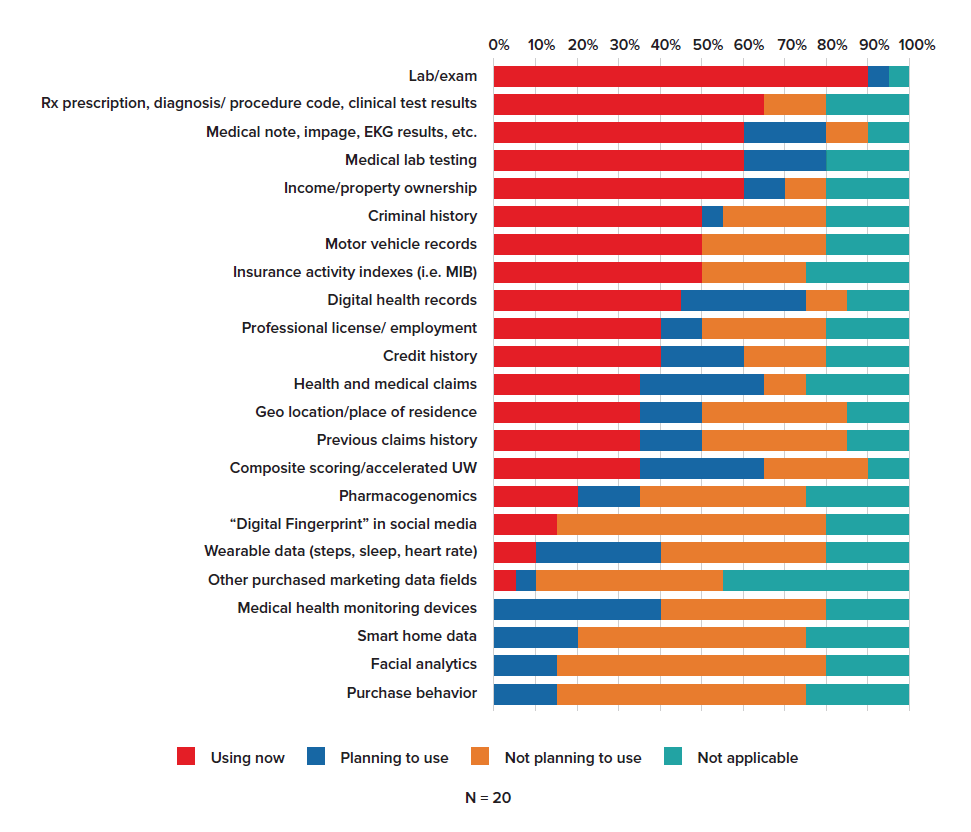

The sources of evidence for underwriting are no doubt broad. In our survey, somewhat unsurprisingly, insurers reported greater use of common or more traditional data sources. Ninety percent of participants are using lab data today and 65% are using prescription drug data. Interestingly, participants also reported a changed view of emerging data sources going forward. For example, 40% of respondents indicated that they are planning to use medical health monitoring devices in the future as an alternative source of evidence. Digital health records are already used as a data source by 45% of respondents, with another 30% intending to use these records in the future. Composite scoring (blending multiple risk scores together) is used by 35% of respondents, with another 30% intending to use it in the future.

Facial analytics, smart home data, and consumer purchase behavior were among the least broadly used evidence sources, with many in the survey group indicating no use of such data today and no plans to use those data sources in the future.

Figure 14:

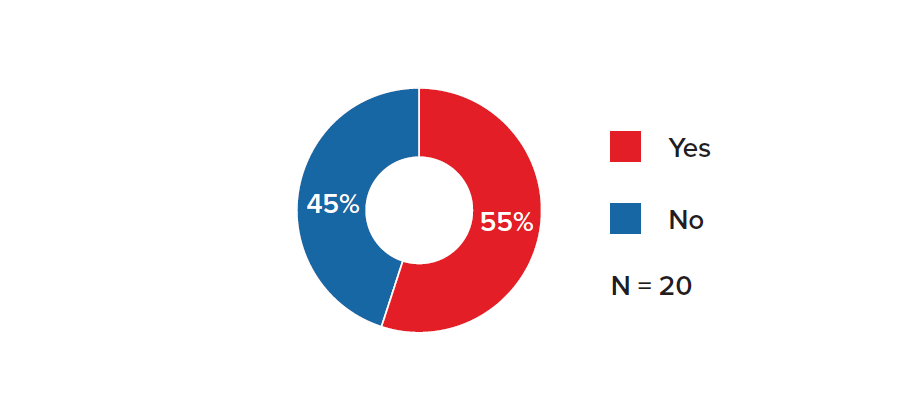

When surveyed about cross-selling/upselling new offerings to existing clients, insurers indicated they are still not fully utilizing the power of their own data to make predictive offers to their in-force book. Fifty-five percent of those surveyed are not using predictive analytics to target marketing efforts for cross-selling or upselling, which is consistent with results from our 2017 survey.

Figure 15:

Managing fraud

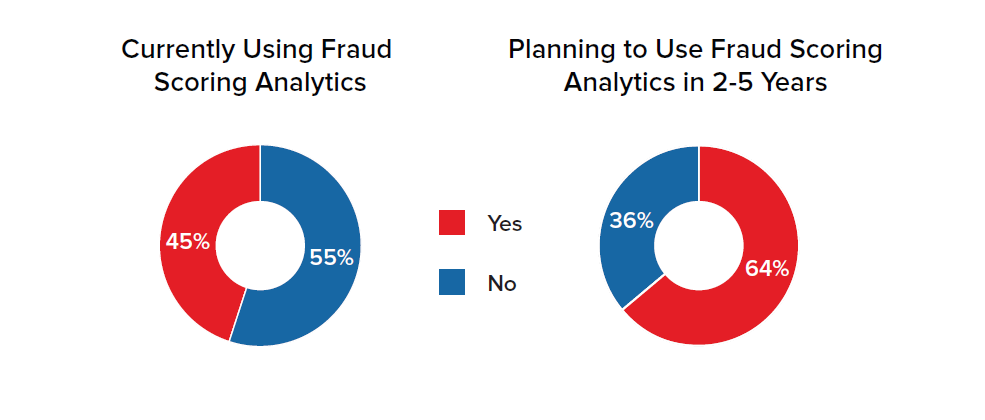

The topic of managing fraud at point of sale has always been top of mind for head underwriters. Our most recent survey findings clearly revealed that more insurers are considering the use of fraud scoring analytics to identify at-risk applicants compared to the 2017 survey. The percentage of respondents using fraud scoring rose from 12% to 45%. Among those not using fraud scoring analytics today, 64% indicated they plan to do so in the future. Click rates and URL locations played a role in the models employed. Some insurers had an internal unit that provided a score to flag specific applications.

Figure 16:

Going forward, in the post-COVID environment where some insurers may be relaxing underwriting requirements on a short-term (or even long-term) basis, managing fraud is expected to grow in importance to counterbalance the propensity for anti-selection and fraudulent activity in the “new normal” environment.

Distribution and focus on the consumer

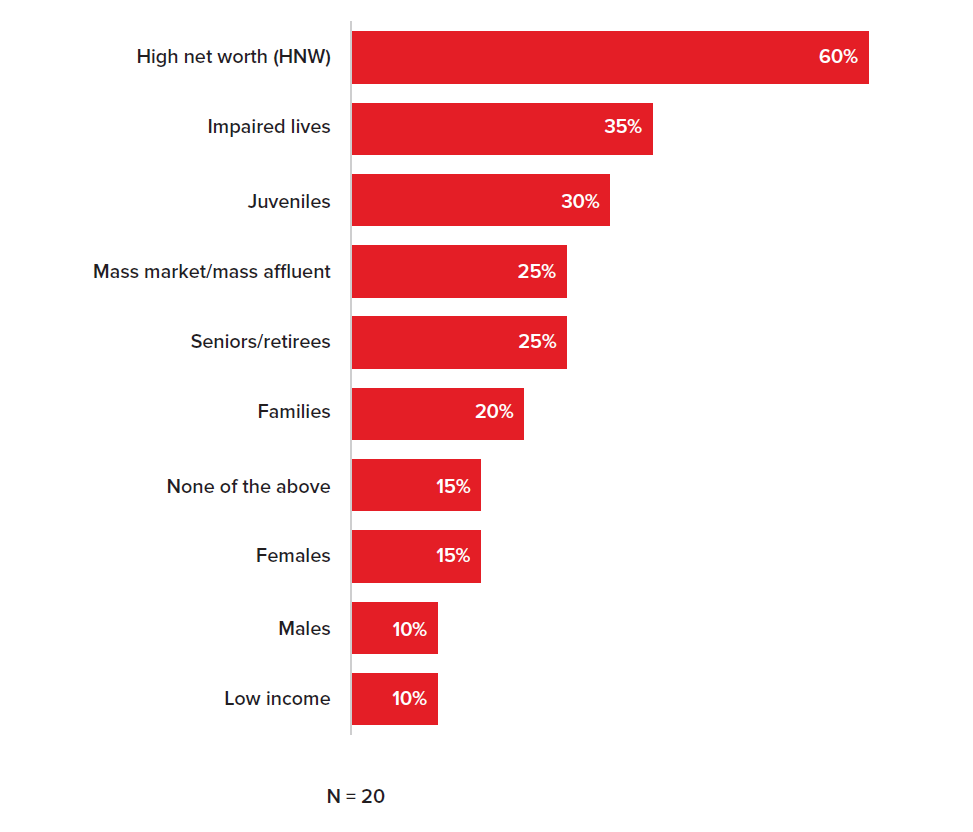

As many insurers continue their pivot to a consumer-centric approach, the drive is on to be less reliant on “one-size-fits-all” products and underwriting approaches. Survey results indicated that the high net worth segment receives the most attention, with 60% of respondents reporting they have or plan to have a formal unit in place to manage underwriting for that segment. Another target was the “impaired lives” market, or those with chronic conditions, at 35%. This was followed by juveniles with 30% of responses. These figures indicate that these segments drew significant attention, compared to the 2017 results of 21% and 21% respectively. RGA’s client engagements suggest impaired lives, juveniles, and similar niche segments receive varying levels of attention depending on geography.

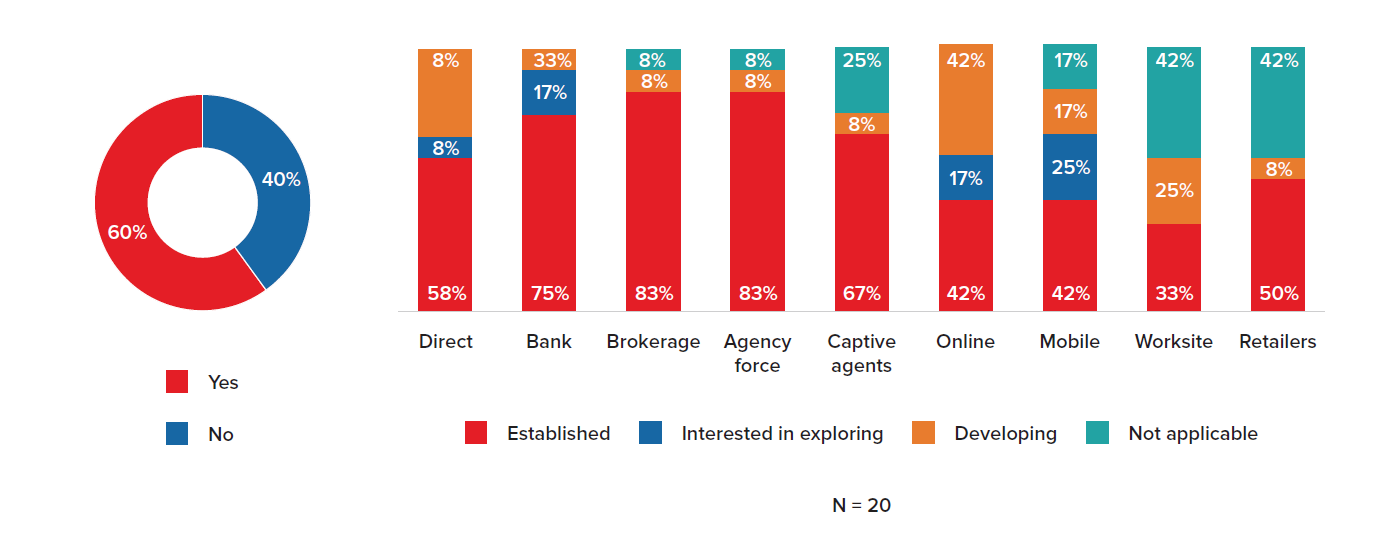

Three-fifths of responding insurers reported tailoring underwriting practices by distribution channel. Online and mobile channels captured the greatest interest among insurers who also prioritized targeted underwriting and “selling at a distance.”

Given this survey was conducted pre-pandemic, we would expect this figure to jump in the weeks and months ahead as face-to-face selling gives way to virtual approaches.

Figure 18:

Synthesizing the findings

The findings of the survey indicate that transformation is gathering speed in underwriting departments at large, multinational life and health insurers. We have noted overall growing urgency for change within the underwriting function, with some plateauing indicating that transformation has just become part of the “new normal.”

The findings demonstrate that now, more than ever, underwriting can provide a competitive advantage. Insurers are finding creative ways to automate underwriting, incorporate increasing amounts and types of data, improve consumer-centricity and cost efficiency, and mitigate fraud during the normal course of business. While electronic underwriting forms the core of an insurer’s digital transformation strategy, our survey participants told us that higher STP rates can only be achieved through a broader digital risk selection and management strategy.

RGA would like to sincerely thank all participants for their time in responding to this survey. We hope you find the analysis and insights informative as you continue to refine your approach to this critical function.

.png?sfvrsn=86c7aef6_0)

5d8a64c4-40be-43b0-a692-a38f20063213.png?sfvrsn=c848acc3_3)