While wellness programs in life and health insurance are nothing new, their effectiveness remains a topic of much debate.

These programs are intended to improve overall wellbeing and increase participant engagement, but accurately measuring their ability to reduce insurance claims has proven difficult. At RGA, we have actively sought to determine the effectiveness of wellness programs and appropriate methods of measurement. In the process, we have identified a core set of facts and evidence-based beliefs to guide our efforts as we help our clients navigate this still promising area of insurance product enhancement.

What do we know?

- We expect better mortality experience for those who are physically active relative to those who are inactive.

- Behaviour change is hard, and many wellness programs struggle to increase healthy activity that results in long-term health improvements.

What do we believe?

Even without behaviour change, insurance-linked wellness programs can improve insured mortality experience. We believe insurance products with a wellness benefit:

- will attract healthier people compared to products without a wellness component

- will retain healthier people compared to products without a wellness component

- can incentivize healthy people to maintain their health

- can improve the activity of some policyholders, with the most profound mortality impact among older people and those with chronic conditions

We know...

Physical activity improves mortality experience.

RGA analyzed health survey data from the U.S. Centers for Disease Control and Prevention (CDC) to quantify the impact of lifestyle behaviours and mortality experience. Based on that analysis, we expect better mortality experience for those who are physically active relative to those who are inactive.

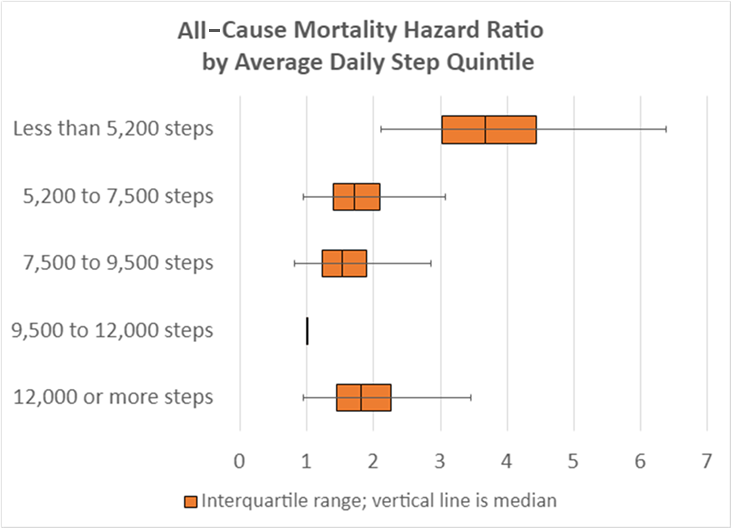

The all-cause mortality ratios shown in Figure 1 segment mortality risk according to quintiles of measured activity with a reference category of 9,500-12,000 average daily steps. Those in the lowest quintile of steps per week – walking less than 5,200 steps – had the highest mortality.

Figure 1: All-Cause Mortality Hazard Ratios by Average Daily Step Quintile

Multivariate model adjusts for: age, sex, smoking, disease history, health status, income, and ability to walk a quarter mile. Source: RGA analysis of NHANES III 2005-2006 survey data. [1]

Exercise, especially vigorous exercise, is more important as we age.

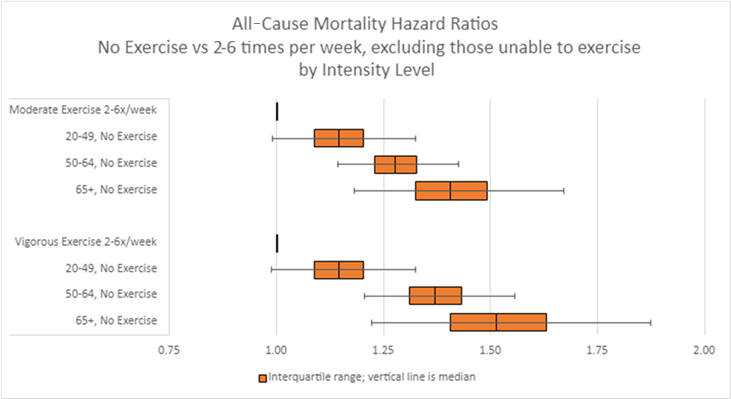

Findings in Figure 2 demonstrate the mortality experience of different age groups who do not exercise relative to the mortality of members of that same age group who exercise 2-6 times a week. The top set of bars compares moderate exercise by age, while the second set of bars compares vigorous exercise by age. Hazard ratios for those who do not exercise increase with age for both moderate and vigorous exercise intensity, indicating that physical activity is more important as we age.

Figure 2: All-Cause Mortality Hazard Ratios by Intensity Level

Multivariate model adjusts for age, sex, smoking, disease history, health status and income. Source: RGA analysis of NHIS data, 1987-2014. [2]

Behaviour change is hard.

Multiple studies suggest wellness programs can change behaviour:

A study by the Rand Corporation found that the Vitality Active Rewards with the Apple Watch benefit achieved sustained, improved activity levels. Tracked activity increased for the most active as well as obese participants and persisted over the 24-month watch payback period. Participants in the program engaged in 34% more activity, equivalent to nearly five days of extra physical activity each month.

Similarly, the AIA Vitality Active Benefits Program found an 18% increase in physical activity in members after "active benefits" were introduced, with the most significant increase in physical activity for people over age 50.

Humana’s Go365 five-year study also found improvements in healthy behaviour. Relative to the first two years of the program, years 3-5 saw a greater number of members eating healthier foods, exercising more, and reducing tobacco use.

- The number of members who ate five or more servings of fruits and vegetables daily rose by nearly 12%.

- The number of members who exercised for at least 150 minutes each week rose by 25%.

- Members were 2.3% more likely to be non-smokers

Other studies question the effectiveness of wellness programs:

The often-cited Illinois Study found little evidence of benefits in the first year from a workplace wellness program as measured by lower health costs, fewer sick days, extra trips to the gym, or rise in productivity.

A 2019 randomized trial involving 32,974 employees at a large U.S. warehouse retail company found that participation in a wellness program resulted in no significant differences in clinical markers of health, healthcare spending or utilization, absenteeism, tenure, or job performance after 18 months.

Given the lack of consistent evidence of wellness program effectiveness, what conclusions can we draw about the potential for wellness programs in life and health insurance? At RGA, we have reviewed the evidence and reached one primary conclusion: Even without behaviour change, wellness programs can improve insured mortality experience.

We believe...

Wellness programs attract healthier people.

Evidence suggests that insurance products with a wellness benefit attract healthier people than products without a wellness component. The Illinois Study showed a strong correlation between workplace wellness program participation and both lower medical expenditures and healthy behaviours. However, the study did not find significant causal effects, suggesting that wellness programs could serve as a screening mechanism for recruitment or retention of lower-cost participants even in the absence of direct health savings.

Wellness programs retain healthier people.

Data indicates that insurance products with a wellness benefit retain healthier people than products without a wellness component. According to Discovery’s 2019 Annual Report, Vitality’s program lowered life insurance lapse rates by 15%. Lapse rate improvements increased relevant to Vitality status: Those with higher engagement exhibited better lapse experience.

Likewise, results from the AIA Vitality program in Australia show that participants in the wellness program were 40% less likely to lapse on their policy than those not on AIA Vitality.

Wellness programs can help maintain good health.

Consumer feedback suggests insurance products with a wellness benefit can incentivize healthy people to maintain their health. A Global Atlantic survey of American consumers found that most survey respondents indicated they would maintain their current weight and visit the doctor for annual check-ups if offered a life insurance premium discount.

People typically gain weight and exercise less as they age. A program that helps people maintain their activity would therefore improve health outcomes even without changing behaviour.

Wellness programs can improve activity levels.

Studies show that insurance products with a wellness benefit can improve the activity of some policyholders, which is especially impactful for older people and those with chronic conditions.

A recent article published in JMIR Diabetes found that Virgin Pulse's "Transform for Prediabetes" digital diabetes prevention program was effective at reducing participants’ risk for developing type 2 diabetes.

In 2015, Aetna conducted a study of a wellness program designed for employees with an increased risk for metabolic syndrome. The results were uniformly positive – 76% of participating employees lost an average of 10 pounds, and trends showed improved clinical outcomes relative to three of five metabolic factors.

A 2019 study of Vitality's Active Rewards intervention program found pronounced improvement in physical activity, especially in the group that stood the most to gain: the least physically active.

- Program participants with low or moderate activity at the start of the program exhibited a dramatic increase in active days that was sustained over the two-year period of the program.

- The least active participants increased their physical activity to more than three times the physical activity recommended by the WHO.

- The least physically active members also experienced the greatest improvements in relative risk of mortality.

Final Thought

While detractors can point to select studies indicating the shortcomings of wellness programs to date, a range of evidence supporting the many health and mortality benefits of participation in these programs demonstrate the value and the potential of continuing to incorporate wellness into insurance offerings. In addition to better health, wellness programs also promote a healthier pool of policyholders, who are less likely to make claims in the future, enabling insurers to pass the savings back to policyholders through discounted premiums or program rewards. In other words, for both insurer and insured, the case for wellness remains strong.